Geopolitical Risks at the Forefront

Geopolitical risks are back to the forefront with the recent Russian invasion of Ukraine. The situation continues to be fluid however, the escalating conflict has had a profound impact on global capital markets, as prices of commodities from oil to wheat soared while stock markets plunged. Western governments have widely condemned Russia’s actions and as a result are imposing crippling sanctions on its financial, technology and aerospace sectors. Market participants are yet to assess the full and wider implications of this ongoing crisis which is heavily affecting global trade and is expected to further exasperate global supply pressures already seen following the pandemic. As the situation develops, we expect the sanctions to intensify, which should place additional upward pressure on energy and commodity prices. The magnitude of the shock is expected to have widespread implications for global growth and inflation which is already at a multi-decade high.

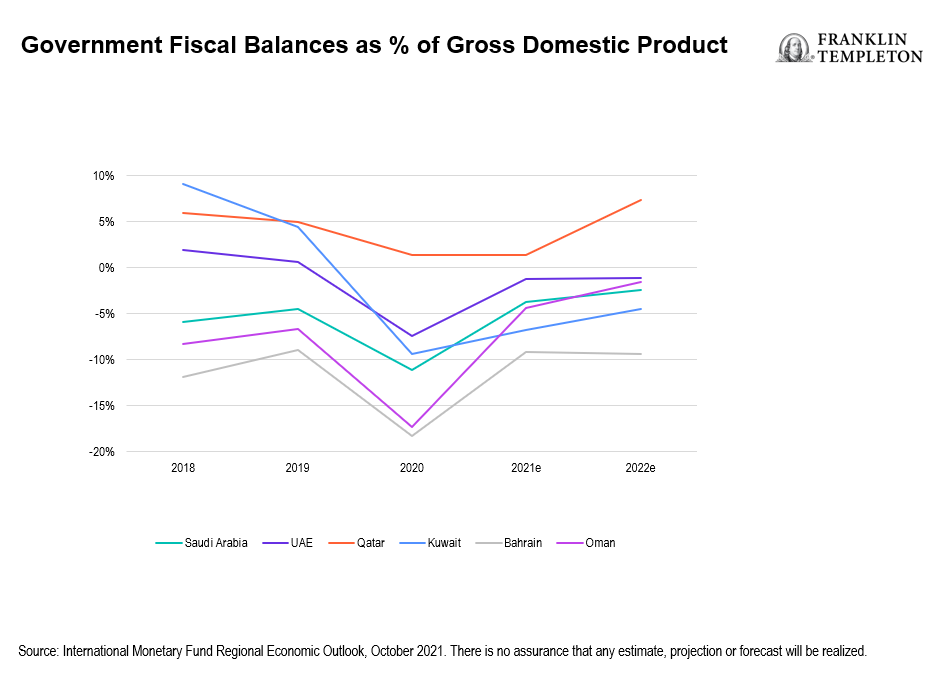

Despite the recent turmoil, Gulf Cooperation Council (GCC) markets have performed strongly. Large sectors within our markets are exposed to commodity and energy prices and stand to benefit from the sharp rise in prices given their low cost base. Moreover, higher oil prices are expected to support government fiscal budgets which should enjoy record surpluses after years of consolidation and reform. We expect fiscal policy to remain prudent and do not foresee an increase in government spending over the short term. Oil windfalls will be channeled to repair balance sheets, reduce debt levels, and improve overall liquidity in the system.

Aside from the Russia-Ukraine conflict, we have identified five key themes for MENA equity investors to watch in 2022:

- Pandemic risks persist, yet are expected to be short-lived

- Higher oil prices should support growth and public investment

- Regional/intraregional politics continue to provide uncertainty

- Higher interest rates bode well for the overall banking sector

- There appears to be ample liquidity to support a healthy initial public offering (IPO) pipeline

Pandemic Risks Persist, Yet Are Expected to Be Short-Lived

In our view, the Omicron variant represents a risk to near-term growth across the region; however, high vaccination rates in the larger MENA countries combined with lower hospitalization rates from the variant suggest that the scale of economic disruption should be lower than previous waves. Saudi Arabia and the United Arab Emirates (UAE) have in fact ruled out strict lockdowns1 as they try to balance economic activity through appropriate restrictions and additional vaccinations. Additionally, fourth-quarter 2021 and early 2022 mobility trends for retail and recreational places have been running 15%–20% above the pre-pandemic baseline in the UAE, Saudi Arabia and Egypt, as opposed to being 20%–30% below baseline in the United States and the United Kingdom.2 We expect further normalisation of economic activity in 2022 supported by improving demand, stronger tourism and higher oil prices.

Higher Oil Prices to Support Growth and Public Investment

The World Bank forecasts real gross domestic product (GDP) growth to accelerate in the GCC region and Egypt during 2022, at a time when major global economies are expected to witness tapering growth.3

We believe, however, that growth won’t be uniform across MENA countries and sectors. Saudi Arabia is seeing a rebound driven by pent-up demand, higher oil output and accelerating domestic investments. Qatar is getting ready to host the first FIFA football tournament in the region during late 2022 and thereafter embark upon its ambitious liquefied natural gas (LNG) expansion. The UAE is benefiting from a tourism-led recovery with the ongoing EXPO 2020, along with strong visa and social reforms. Egypt is resuming its growth path while managing inflation and currency pressures. Accordingly, we deem 2022 as a year that should see equity investors focusing on earnings trajectory after enjoying a recovery rally in 2021.

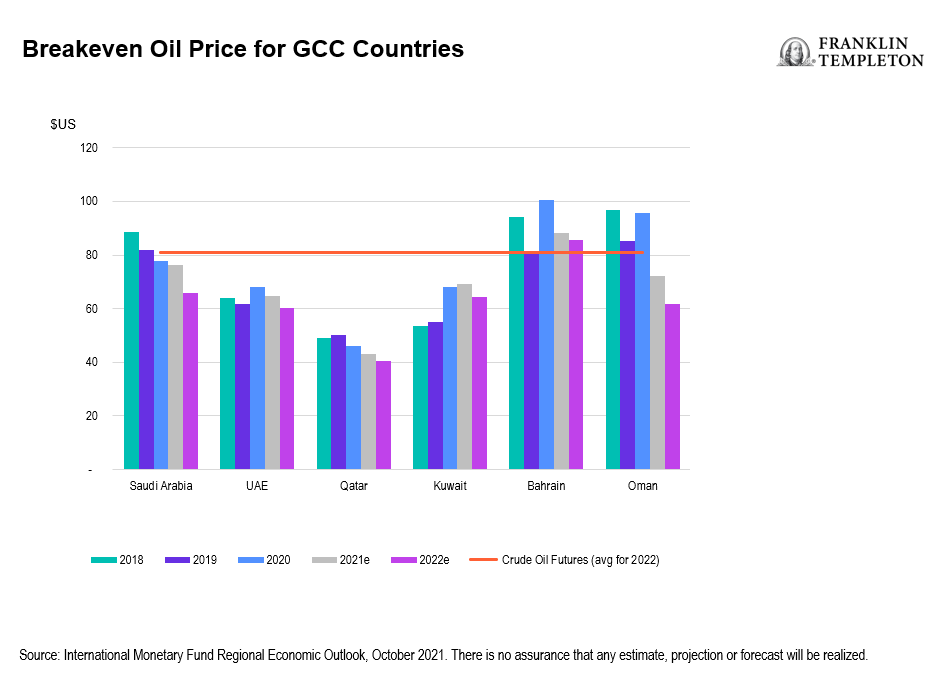

Volatility notwithstanding, oil prices rebounded in a significant way during 2021, with average Brent crude oil prices climbing 64% year-on-year (y/y) to end the year at US$71 per barrel. A combination of reform initiatives over the past few years, along with higher oil prices currently, is translating into significantly improved fiscal positions for the region’s economies. The fiscal breakeven oil prices for many GCC nations have been on a persistent declining trend during last three years, led by efficient spending, taxation changes, subsidy removals and privatization.

The tailwinds of past reforms have become more pronounced with an improved oil price scenario, alleviating the debt burden for challenged economies in the region such as Oman and Bahrain, while providing liquidity boost to others like Saudi Arabia and Qatar. This has enabled governments to accelerate the growth agenda of their non-oil economies without risking fiscal consolidation goals, such as Saudi Arabia’s Public Investment Fund’s (PIF’s) recently announced plan to inject US$40 billion in the country during 2022 (vs US$22 billion during 2021).4

For countries with a low debt burden and a strong foreign exchange (FX) reserves position, higher oil prices also offer the latitude to partially roll back some of the tough measures imposed during the pandemic (such as the tripling of the value added tax in Saudi Arabia) and stimulate consumer spending. As such, we expect the benefits of higher oil prices to spill over into the non-oil sectors.

Regional/Intraregional Politics Continue to Provide Uncertainty

Last year was an eventful one for regional politics. The Abraham Accords, the Gulf-Qatar détente, the Saudi-Iranian dialogue and the Emirati-Turkish rapprochement are amongst the positive developments during 2021. However, we remain cautious about the geopolitical outlook for 2022. The spotlight will be centered on an Iranian nuclear deal and Iran’s relationship with the broader region. We see a successful conclusion to the nuclear talks as highly positive only if broader regional security questions are resolved as well. The trend towards rebuilding relations damaged over the past few years and normalizing ties between key MENA countries will likely continue. The rapprochement between Turkey, Egypt, Qatar, Saudi Arabia and the UAE will likely progress slowly, as countries cooperate and establish deeper-rooted ties in security and trade.

While the GCC is united in trying to ease regional differences, there is healthy internal competition emerging aimed at advancing individual national visions and ideologies. Efforts to build economic diversification away from oil have gathered momentum in recent years, in light of increasing oil price volatility and environmental concerns. Set against this backdrop, economic competition has intensified recently. Saudi Arabia’s bid to increase inward investment into the kingdom in an effort to prevent economic leakages. Most notable amongst these has been the prioritization of talent attraction. At the same time, the UAE has promoted human capital by introducing several types of residency visas for skilled workers and those with special talents. However, what has been unfolding is a rapid acceleration of social and economic reforms, leading to a healthy competition that we expect to be net accretive for the region.

Higher Interest Rates Bode Well for the Overall Banking Sector

GCC banks’ profitability typically benefits from an upward trajectory for interest rates. Currency pegs to the US dollar mean that GCC central banks generally follow the direction of the Federal Reserve’s policy rates, which should lead to expansion in net interest margins for GCC banks. On average, a 100 basis-point (bp) increase in policy rates would result in a 14% earnings boost and 1% capital accretion.5 All else being equal, gradual rate hikes are unlikely to squeeze loan growth given a backdrop of sovereign-led stimulus. Credit growth should remain robust in 2022 in Saudi Arabia, with continuity of mega projects, the Shareek Programme and the Kingdom’s mortgage law. Kuwait is also planning to roll out a new law to boost mortgages, while gas-related investment is picking up in Qatar. Higher oil prices should support system liquidity as well as lending. Consequently, credit activity in the GCC is expected to witness higher growth than seen in the past five years. Growth recovery is also conducive for a benign asset quality outlook and controlled credit risk costs, further supporting banking sector earnings.

In Egypt, we see rate hikes having no impact due to the short-term nature of both deposits and assets. Higher interest rates there should help maintain the attractiveness of the carry trade of Egyptian treasury bills, providing support for the stability of the Egyptian pound. This is even more important in the current environment given the uncertainty around the quantum of tourism recovery, and while the Fed is instead looking towards tightening.

Ample Liquidity to Support a Healthy IPO Pipeline

Regional markets saw a resurgence of liquidity in 2021 driven by a sharp economic recovery, a bounce back in oil prices, a pickup in overall sentiment and a continuation of critical reforms. Sidelined capital made a comeback, setting the stage for a flurry of IPOs in Saudi Arabia, the UAE and Egypt. The listings have come in a range of sectors, adding approximately US$7.5 billion6 to regional markets’ float. Performance has generally been strong, with an average return of over 30% since listing,7 reflecting the appetite for further investment.

This year is shaping up to be one that builds on the successes of 2021, further broadening the MENA investment universe and expanding companies’ access to capital markets. Dubai is leading the way and has announced plans to rejuvenate the local market with 10 state-related entities expected to list. The UAE is also motivating large family-owned businesses to list. We expect similar healthy pipelines in various countries such as Saudi Arabia and Egypt as well.

Valuation Premium Justified by Growth Outlook

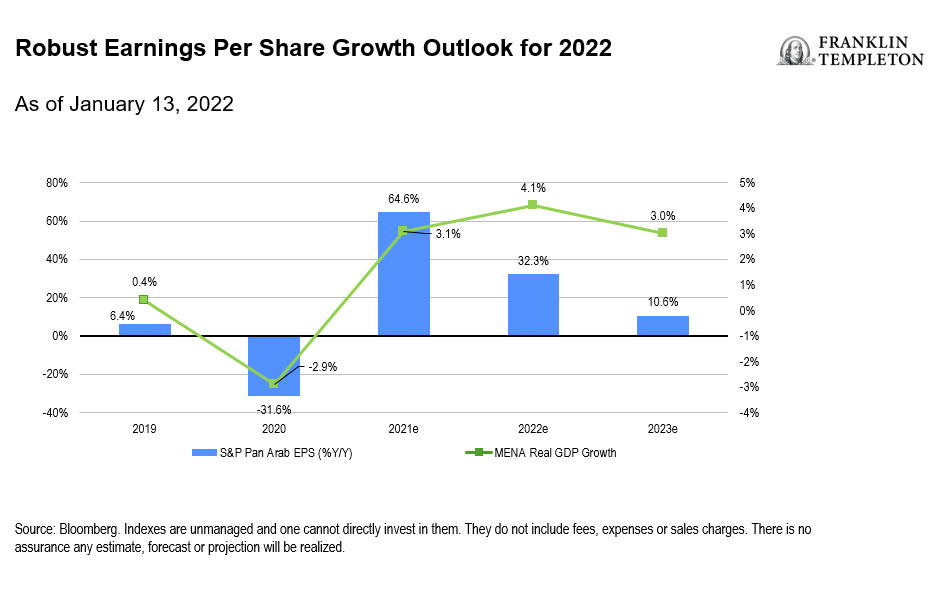

MENA markets were amongst the top performers during 2021, with the S&P Pan Arab Composite Index returning 32.6% net. In comparison, the MSCI indices for developed markets, emerging and frontier markets returned 22%, -3% and 20%, respectively.8

A sectoral breakdown of 2021 performance shows the largest contribution coming from industrials and financials, while consumer staples and information technology lagged the most after a solid 2020. For 2022, we continue to see tailwinds for consumer recovery, as well as health care sectors, while financials should see renewed interest outside of Saudi Arabia.

MENA valuations sit higher versus historical averages and relative to emerging markets, though they appear well supported by the real GDP outlook, earnings trajectory and US dollar-pegged currencies. We believe current valuations, taken at face value, mask a high level of dispersion between different sectors and countries. Saudi Arabia, Abu Dhabi and Kuwait all have been trading at the higher end of their historical ranges on both price-to-earnings (P/E) and price-to-book (P/B) multiples—all three markets have seen substantial improvements in liquidity over the past two years, and the former two have had busy IPO calendars.

Amongst the other major markets, Qatar, Dubai and Egypt are still relatively cheap compared to their historical levels. We believe their markets are positioned to perform well on the back of attractive valuations and the ongoing recovery in overall demand. Amongst sectors, we favor financials, health care and consumer discretionary. We are less constructive on materials given the runup in valuations and the decreasing product margins.

What Are the Risks?

All investments involve risks, including the possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realised. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

______________________________________

1. Source: Arab News, “Saudi Health Ministry rules out stricter lockdown amid COVID 19 case surge,” 4 January 2022.

2. Source: Our World in Data, as at 12 January 2022.

3. Source: World Bank, as at 11 January 11, 2022. There is no assurance that any estimate, forecast or projection will be realized.

4. Source: Arab News, “Saudi PIF to invest $40bn locally in 2022, says Crown Prince Mohammed bin Salman,” 13 December 2021.

5. Source: S&P Global Ratings GCC Banking Sector Outlook, 11 January 2022. One basis point is equal to 0.01%.

6. Source: Franklin Templeton calculations based on data collected for various IPOs.

7. Source: Bloomberg. See www.franklintempletondatasources.com for additional data provider information.

8. Source: Bloomberg. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results. See www.franklintempletondatasources.com for additional data provider information.