By Franklin Templeton Emerging Markets Equity

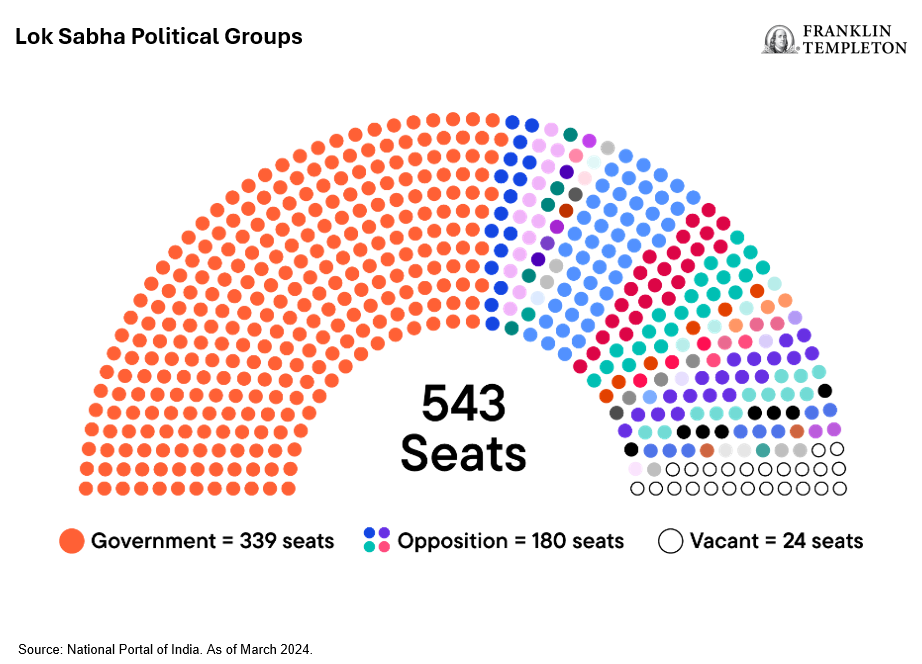

India will go the polls on April 19, with voting in the general election continuing over six weeks, concluding on June 1. The incumbent Bharatiya Janata Party (BJP), led by Prime Minister Narendra Modi, is expected to win comfortably. Investors are focusing on whether the party and its partners can win 358 seats—or a two thirds majority in the lower house—which will enable them to make constitutional changes. In the 2019 general election, the BJP won 303 seats, versus 52 of the 543 seats won by the opposition Congress party.

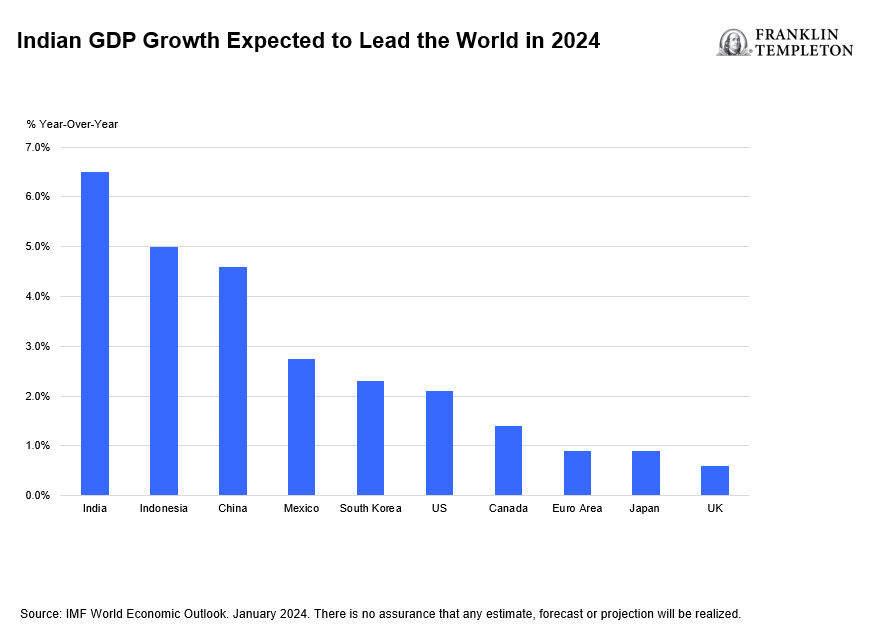

A combination of factors is driving investor confidence in a BJP win. The party maintains a solid economic record, with this year’s gross domestic product (GDP) growth the highest among large global economies. The party is also well organized. Party representatives will be present at the majority of the one million polling stations in India, where 969 million voters cast their votes. The party also has a record of meritocracy in selecting candidates, which creates an inclusive environment and reduces the risk of internal splintering.

A two-thirds majority of votes for the BJP and its partners will enable Modi to make constitutional changes, addressing some of the biggest concerns among local business and foreign investors. These include unifying the timing of local and national elections, versus the current practice of state elections being held at various times over the year. This could boost productivity as state elections are deemed holidays. There is also the possibility of boosting the government’s ability to raise additional tax revenue with judicial and economic reforms.

Conservative fiscal policy

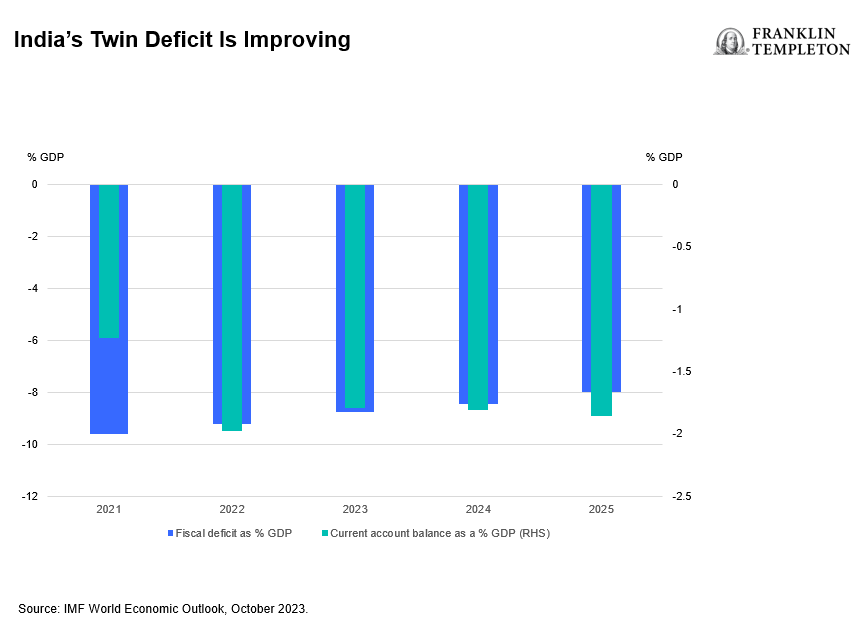

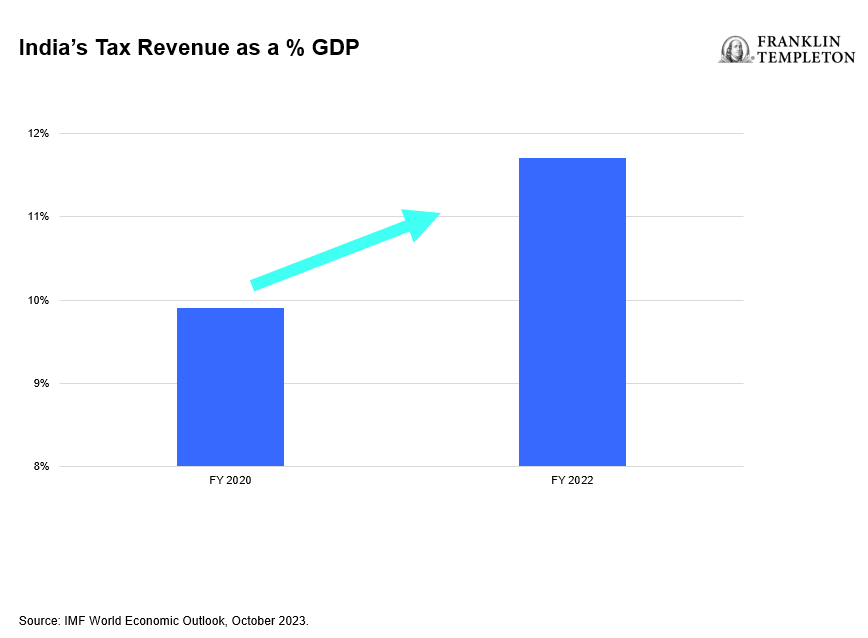

If he wins a third term, Modi’s focus on conservative fiscal policies is likely to remain in place. The reform of the goods and services tax in 2017, which has doubled collections to US$180 billion, has increased total tax collected as a percentage of GDP to 11.7% in FY22, up from 9.9% in FY20.1 As such, spending on infrastructure and welfare has increased, and the size of the budget deficit has been reduced.

With rising tax revenues, the government has been able to support green investments and amplify its focus on investment in information technology hardware. Recently there has been a focus on investment in semiconductors, as policymakers seek to increase domestic supply and diversify the technology sectors’ reliance on software services.

“India’s largest population of IT professionals and their AI skills will help lead the AI revolution.” Jensen Huang, CEO NVIDIA.2

On February 29, Modi announced three semiconductor investments totaling US$15 billion. The investments include India’s first wafer fabrication production facility, with an initial capacity of 50,000 wafers per month.3 The plant will be based in Gujarat. These projects will involve joint ventures with leading Taiwanese and Japanese semiconductor companies. In addition, the world’s leading memory chip producer in 2023,4 will invest US$2.75 billion in an assembly and testing facility in Gujarat.

Increased labor-force participation

India has a working age population of 900 million; however, only 45% are in possession of an intermediate education. For women, this falls to 19%.5 Low by international standards, female labor- force participation is 25%.6

Modi has initiated a new education policy focused on reforming laws which are obstacles to increased female participation in the labor force.7 The policies include training and potentially quotas to encourage companies to hire more women. The UNICEF and PWC upskill program will complement this policy. UNICEF will implement, and PWC upskill will finance skills education for 300 million people of working age in India, with a focus on women. The program will address skills shortages and fill the education gap created by the COVID-19 pandemic.8

Targeting developed country status by 2047

A hundred years after its independence, India is targeting developed country status by 2047. Policies to achieve this include Production-Linked Incentives, which were launched in 2020, and the “Make in India” program. Supply-side policies centering on improving infrastructure and the upskilling of the workforce have also been announced.

Assumptions for India to achieve developed market status by 2047:

- Nominal annual GDP growth of 12%

- Current population growth maintained

- INR/USD depreciation of 2% annually through 2025, annual appreciation of 0.5% thereafter

Improving skills and in turn raising productivity are among the most important policies to achieve developed market status by 2047. While these policies may not be as eye catching as urban metro systems or semiconductor fabrication investments, they are no less important. Increasing the educational attainment of India’s young people is vital to reaping the demographic dividend.

India’s “Techade”

Modi speaks about the 2020’s as India’s “Techade.” In the near term, he is focused on expanding domestic demand, while in the medium term, the focus is on raising export capacity. Free trade agreement negotiations are underway with the European Union and the United Kingdom. The India, Middle East, Europe trade corridor is being developed to take advantage of tariff free access to these markets. These supply-side policies are as important as investments in manufacturing capacity to build a long-term sustainable export base in India.

The fiscal year 2023 budget included three policy priorities for India to fulfill its potential in the Techade ahead:

- Promoting a digital economy, focusing on technology enabled development and energy transition

- Creating a virtuous circle of public and private investment to “crowd in” private investment

- Micro economic reforms focused on expanding welfare programs for the poor

Equity-market implications

The focus on investment and raising educational attainment will contribute to the expansion of India’s middle class, ideally lifting millions out of poverty. Companies in the consumer discretionary sector are likely to be beneficiaries of these policies. Our on-the-ground research has also identified opportunities in the health care sector, both in the production of pharmaceuticals and healthcare providers. We also see opportunities in the real estate sector, particularly with companies with balance-sheet strength.

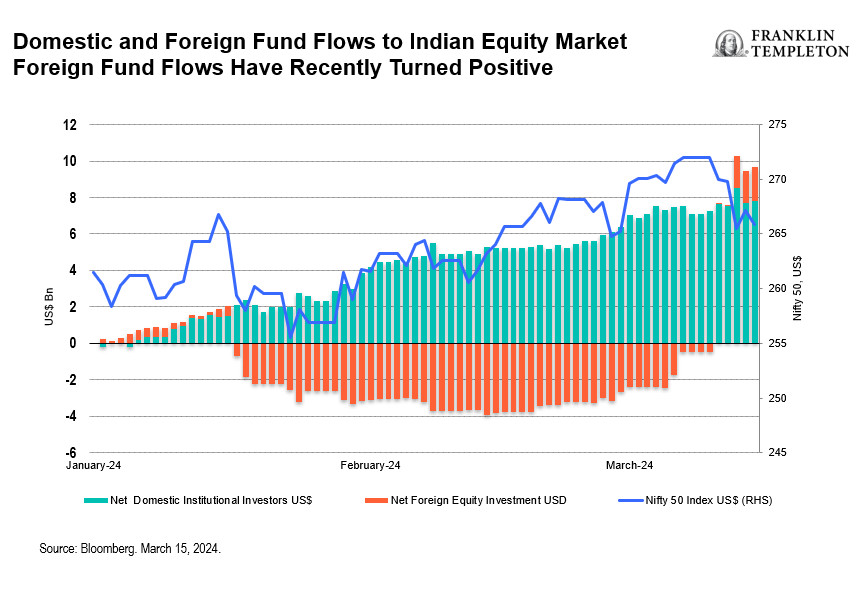

Foreign institutional investors have recently joined local investors in buying into the India Techade theme, with flows turning positive in March 2023 following a period of foreign fund outflows. Domestic investors have remained resolutely positive this year.

What to watch for

If the BJP wins the upcoming Indian general election, we do not expect any significant changes in government policies. Modi has set out his vision for achieving developed market status by 2047 and will focus on the continued implementation of policies to achieve that goal. If he achieves a two-thirds majority in the election, he will have a mandate for constitutional change, which may include judicial and election reform. These should be broadly positive for investors.

Risks for investors center on the implications of the successful execution of Modi’s economic priorities. A “winner’s curse” could see India’s export ambitions curtailed by an appreciating exchange rate. The INRUSD exchange rate depreciated by 35% over the past 10 years. This was due to a combination of a rising current account deficit and a wide inflation differential with peers, necessitating a weak exchange- rate policy to maintain export competitiveness. In our view, any future exchange rate appreciation is likely to be gradual, so policymakers can liberalize the capital account in stages to manage the upside.

Looking ahead, a reduced dependence on fossil fuel for power generation and a focus on value-added manufacturing for export could result in a currency account surplus, putting appreciating pressure on the INR/USD exchange rate. While import costs would be reduced in this scenario, if India successfully executes its supply side policies, in particular education reform, we believe the country should be able to compete internationally and not rely on a weaker exchange rate.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Investments in companies in a specific country or region may experience greater volatility than those that are more broadly diversified geographically.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

_________________________—

1. Source: Government of India. April 14, 2022

2. Source: NVIDIA.

3. Source: Prime Minister of India’s office. February 29, 2024.

4. Source: Micron Technology. June 22, 2023.

5. Source: International Labor Organization, February 6, 2022

6. Ibid.

7. Source: India Press Information Bureau. July 29th, 2020.

8. Source: PWC. December 7, 2020.