Key takeaways:

- South Korea and Taiwan strongly outperformed most of their peers quarter-to-date.

- A strong US dollar and receding energy prices support solid macroeconomic fundamentals of export-oriented economies.

- Optimism is further spurred by what we consider attractive valuations, positive outlook for the chip and materials industries despite the current demand slump.

- Long-term supply-chain realignments could benefit both economies.

South Korean and Taiwan equities have been among the best performing globally thus far in the fourth quarter of 2022, and we believe for good reason. While their Asian Tiger peers Singapore and Hong Kong returned between 2% and 9% during the quarter, South Korea and Taiwan are up 17% and 12%, respectively.1 Broad emerging markets have risen just under 5%.2

The primary factors driving the recent surge in relative performance appear to be:

- Investor bargain hunting

- Semiconductor chips and electric vehicles (EV) market optimism

- Strong fundamentals

How sustainable is this trend, and is the time ripe for investors to take a closer look? Let’s consider each element driving returns.

-

Bargain hunting

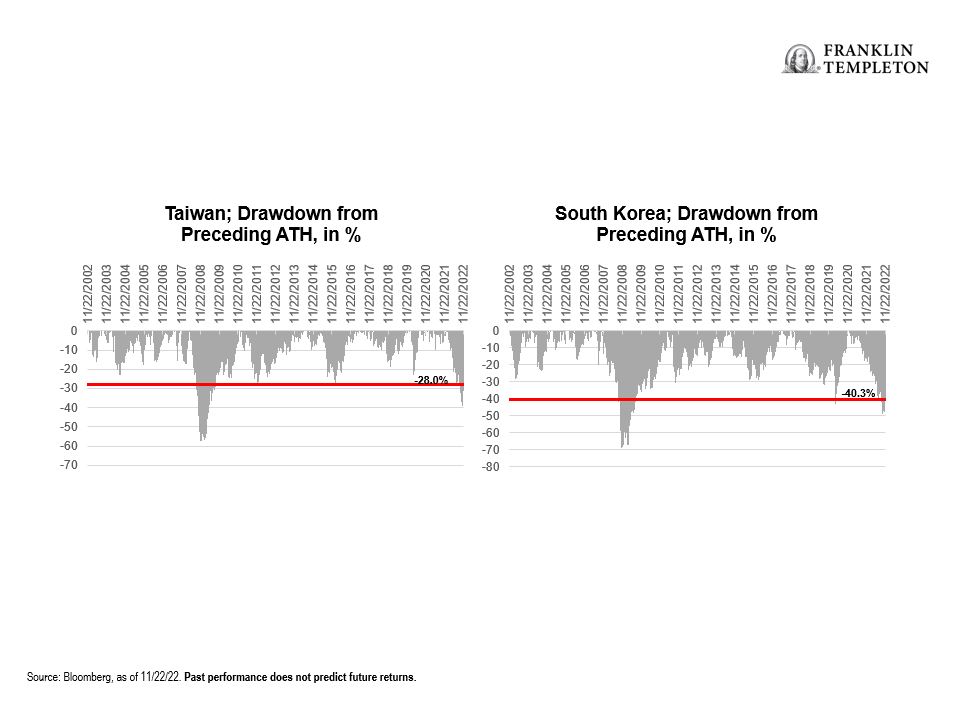

Both markets have recently seen some of their worst drawdowns in at least two decades. As of late November, the FTSE South Korea Capped Index is down 40% from its all-time-high (ATH), while Taiwan’s index has declined 28%. These returns are considerably less than during the Global Financial Crisis, but eclipse bear markets such as the bursting of the Chinese equity bubble in 2015-2016 and the 2018 US-China trade war. Additionally, for Taiwan, its return also surpasses the spring 2020 COVID-19 crash.

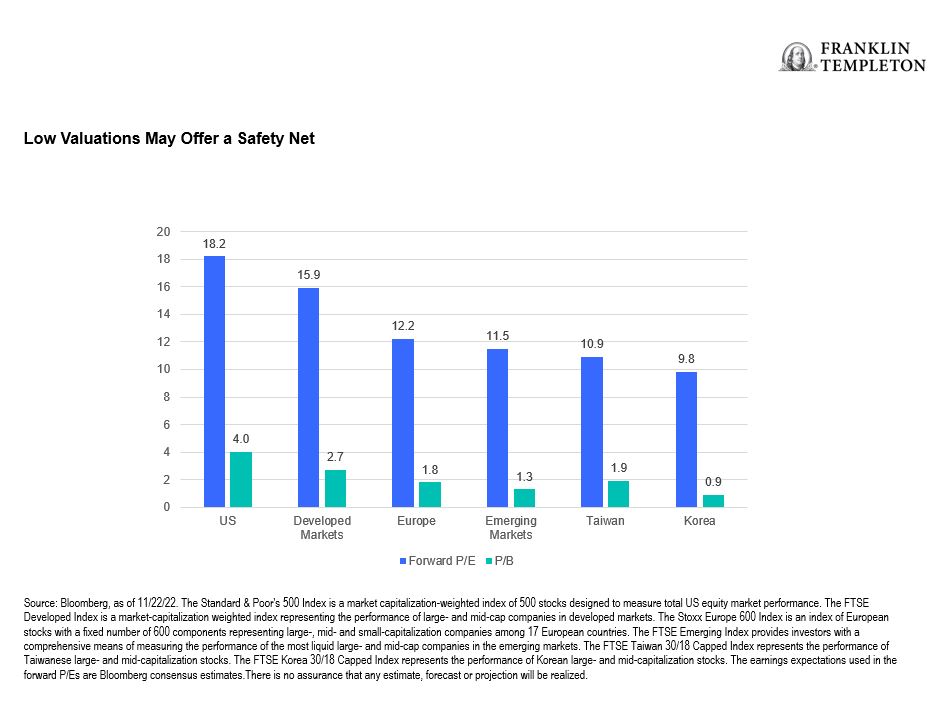

On its own, this development wouldn’t be sufficient reason for us to consider these markets attractively valued. However, even with the prospects of a possible global recession—which is not our base case—we believe comparatively low valuations can offer a buffer if earnings expectations are lowered. While multiples have already retreated from their highs, US markets are still trading at an estimated forward price-to-earnings ratio (P/E) of 18, while South Korea and Taiwan are at 10x and 11x. In our analysis, the discount is even more striking in price-to-book ratio (P/B) terms.3

In perhaps the most notable example of potential bargain hunting, Warren Buffett’s Berkshire Hathaway recently reported a new US$5 billion stake in Taiwan Semiconductor Manufacturing Co. (TSMC). The news came just weeks after the United States set new restrictions on sales of advanced semiconductors to China. The move is primarily intended to hamper Chinese technology capabilities, including military applications of artificial intelligence (AI), but it is also a further step in the “decoupling” of supply chains from China more broadly. The increasingly popular “China plus one” strategy could allow South Korea and Taiwan to pick up some business over the medium term. The recent passage of the US Inflation Reduction Act, which aims to generate investments in domestic manufacturing and encourage procurement of critical supplies from free-trade partners, may have a similar effect—provided Taiwanese and South Korean manufacturers manage to receive the extension on federal tax credits, for which they are lobbying.

Semiconductor chip manufacturing notoriously poses sky-high barriers to entry, driven by enormous capital requirements and technological know-how, maintaining the dominance of the industry’s few major players. TSMC has recently announced preliminary plans to produce advanced chips at its new factory in the western United States (Arizona), though the United States’ global chip manufacturing share remained a mere 12% as of last year (vs. close to 40% in 1990).4

-

Semiconductor and EV market optimism

Bargain hunting can benefit investors in the short term, but for medium- and longer-term outlooks, quality is worth assessing. South Korean and Taiwanese equity markets, both dominant in the information technology sector (namely semiconductors), are also heavily composed of materials and industrials holdings—with weightings currently ranging between 14% and 23%.5

Both markets host leading, highly profitable companies with wide moats and have built a robust ecosystem around them. Taiwanese companies, for example, command some 11% of the world’s liner fleet.6 Given that 80% to 90% of global trade is carried by sea, that is a crucial advantage in times of disrupted supply chains, especially for an export-heavy economy.

Semiconductors: There is some timid optimism that we are nearing the bottom of the chips cycle. After a near-unprecedented chip shortage during 2020 and 2021, this year has seen the squeeze turn into a glut. Over the summer, stockpiles soared and consequently some leading firms have cut planned capital expenditures by as much as 50% for 2023.7 At the same time, we are confident that capacity reductions today can morph into the price hikes of tomorrow—as has so often been the case in an industry known for its pronounced cyclicality. Generally speaking, we believe that if the semiconductor inventory cycle peaks around the turn of the year, the technology sector may have already reached its lows.

Industrials/Materials: With the world shifting more quickly toward EV, battery demand has soared in tandem. McKinsey forecasts the market for battery cells to grow, on average, by more than 20% per year until 2030.8 This bodes well for South Korea’s petrochemical heavyweights, one of which is spending billions to accelerate the sustainable expansion of its battery material production lines, including a recently announced plan to construct a manufacturing facility for EV components in the southern United States (Tennessee).

-

Strong fundamentals

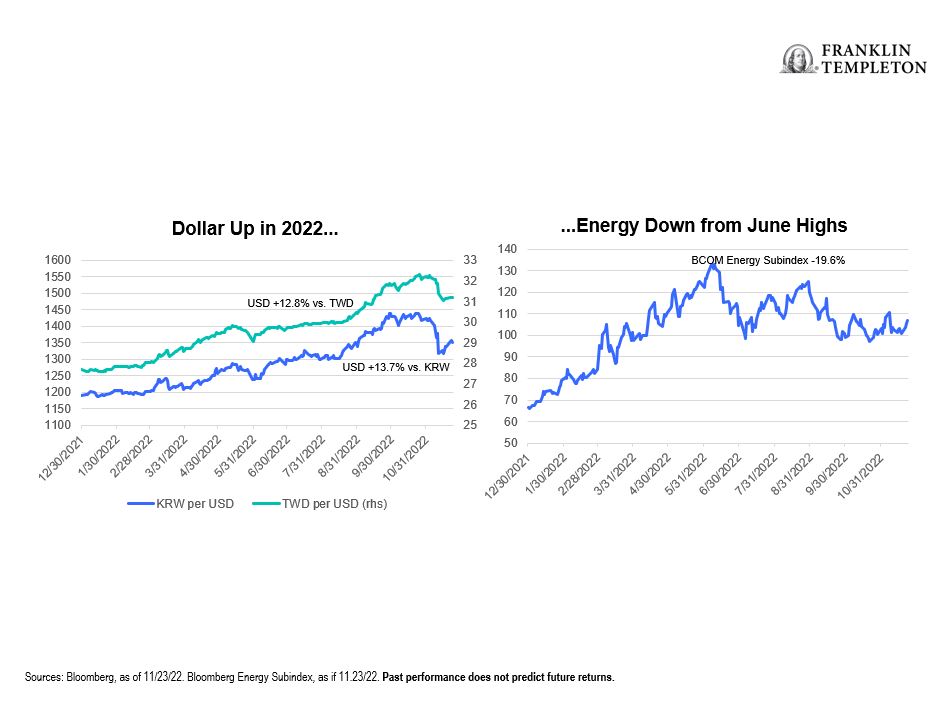

Lastly, we note that both South Korea and Taiwan are in comparatively enviable positions when it comes to macroeconomic fundamentals. As export-oriented nations, they tend to benefit from weaker currencies. While the US dollar strength came to a sudden halt as of late, both the South Korean won (KRW) and Taiwan dollar (TWD) are still significantly cheaper compared to levels seen at the start of the year. Among the more negative effects of a weak currency in either market is the fact that energy imports become more expensive. But with energy commodities down almost a fifth from their June highs, some relief in budgets may appear.

With debt-to-gross domestic product (GDP) ratios of 30% in Taiwan and just under 50% in South Korea, both countries remain well positioned to withstand a global economic downturn in our view. While debt has grown, so have currency reserves that are hovering near all-time highs.

On an annual basis, South Korea’s economy is still growing at close to 3%, despite a weak third quarter with near zero growth. However, while forecasts for 2% growth next year may seem disappointing in an emerging market context, we believe South Korea should still outgrow most advanced economies. The country’s GDP-per-capita is more comparable to developed, not developing, markets.

The country can also benefit from a notably high rate of productivity that serves its “agritech” innovation well, considering still looming food security issues. South Korea has ranked highest in government research and development (R&D) funding for agricultural sciences among OECD nations.9 It also boasts impressive government blockchain initiatives, including plans for blockchain-powered networks to improve transparent food supply chains as well as another game-changer—new blockchain-based digital IDs to be implanted in smartphones and replace existing credentials. Such IDs could potentially transform business and government efficiencies and vastly benefit South Korea’s digital economic foundation and metaverse buildout.10

In conclusion, we think that despite the elevated risks—including geopolitical headwinds—of single-county allocations, overweighting Korean and Taiwanese equities today may benefit investor portfolios given what we believe to be moderate valuations that may be viewed as attractively priced. The Asia region’s standing as the global driver of middle-class growth should also continue to present long-term opportunities, particularly given the world’s imperative green energy transition and technological advancements.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with investing in foreign securities, including risks associated with political and economic developments, trading practices, availability of information, limited markets and currency exchange rate fluctuations and policies; investments in emerging markets involve heightened risks related to the same factors. Investments in fast-growing industries like the technology and health care sectors (which have historically been volatile) could result in increased price fluctuation, especially over the short term, due to the rapid pace of product change and development and changes in government regulation of companies emphasizing scientific or technological advancement or regulatory approval for new drugs and medical instruments. China may be subject to considerable degrees of economic, political and social instability. Investments in securities of Chinese issuers involve risks that are specific to China, including certain legal, regulatory, political and economic risks.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

__________

1. Source: Bloomberg, 2022.

2. Ibid.

3. Source: Bloomberg, 2022. The price-to-earnings ratio is the ratio for valuing a company that measures its current share price relative to its earnings per share (EPS). The price-to-book (P/B) ratio measures the market’s valuation of a company relative to its book value; it’s used by value investors to identify potential investments.

4. Source: Semiconductor Industry Association, “2021 State of the U.S. Semiconductor Industry,” September 2021.

5. Source: FTSE Russell, November 22, 2022.

6. Source: Statista, “Leading ship operator’s share of the world liner fleet as of October, 2022,” 2022.

7. Source: Reuters, “In ‘unprecedented’ global chip slump, SK Hynix to halve investment as recession looms,” October 26, 2022.

8. https://www.mckinsey.com/industries/electric-power-and-natural-gas/our-insights/capturing-the-battery-value-chain-opportunity

9. Source: World Bank, “Digital Ag Series: Fostering Digital Agriculture Ecosystems and Smart Farming in Korea – Case of Smart Farm Innovation Valleys, World Bank Group,” 2021.

10. Source: Korea Post, “RDA shares ‘K-agricultural tech’ with developing countries,” 2022.