Time with loved ones over the new year provides the right perspective to focus on what is important. So, before I dive into my market outlook, allow me to wish you a happy and prosperous new year.

For fixed income, 2022 was one for the record books. Interest rates rose more than most predicted, and inflation continued its decade-long ability to surprise forecasters. Spreads also rose across the board, with few exceptions, and the US dollar was strong against developed and emerging market currencies, leaving little room to avoid financial market pain.

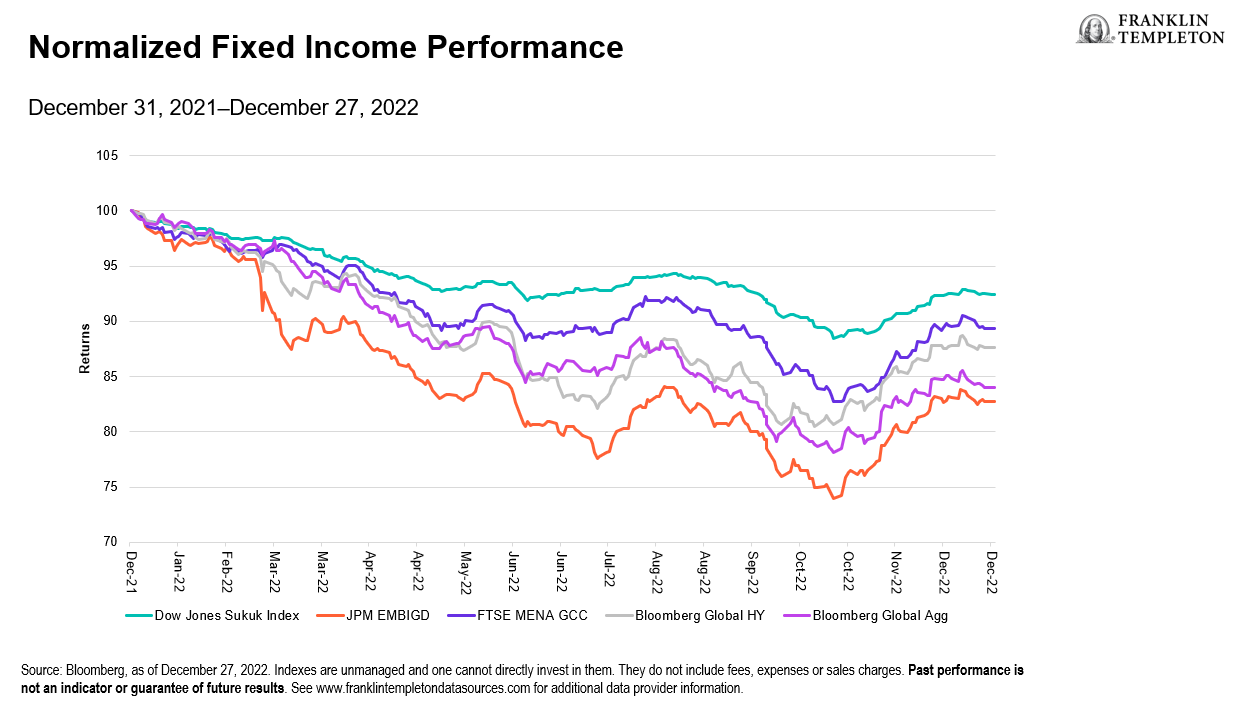

Bonds in the Gulf Cooperation Council (GCC) countries1 as well as global sukuk markets did an admirable job relieving much of that pain. Contrary to most investors’ perceptions of this region and asset class as volatile and risky, GCC fixed income and global sukuk markets delivered on their defensive attributes, declining 61% and 43% of the drawdown of emerging markets, respectively (see Exhibit 1 below)2.

Exhibit 1: 2022 Performance Normalized to 100 on December 31, 2021

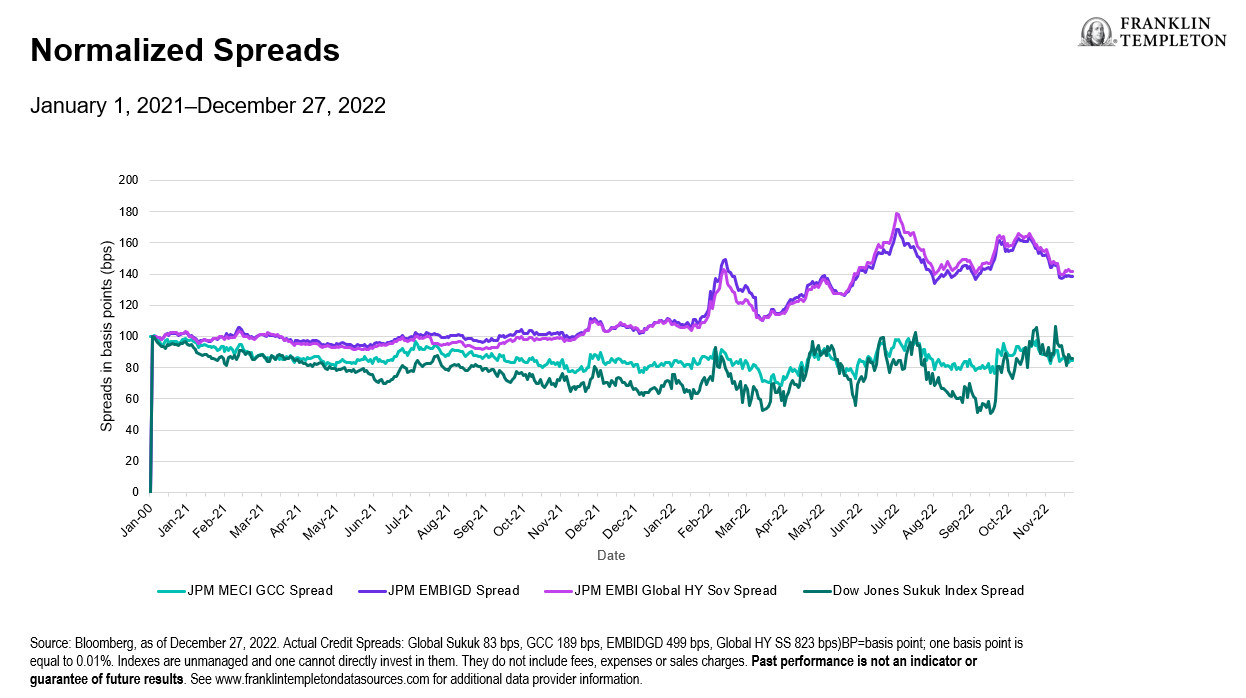

The major reason for this outperformance came from the stability of credit spreads. Whereas spreads across emerging markets widened by as much 80% and currently sit at approximately one-third higher than the beginning of 2021, GCC and global sukuk credit spreads were very resilient, spending much of the past year 20%-40% below their levels of 24 months ago (see Exhibit 2)3.

Exhibit 2: Index Credit Spreads Normalized to 100 on December 21, 2020

Several factors come into play here. Part of this stability comes down to fundamentals. The GCC had a successful public health response to the COVID-19 pandemic and a robust reopening that, according to the International Monetary Fund, came at a fraction (about 1/6) of the cost it took advanced markets to engineer the same recovery (1.5% versus 7.5% of their 2020 gross domestic product as a fiscal response to COVID-19).4

Ukraine and Russia are remote from the GCC and the linkages are limited, which together with higher oil prices, supported the relative strength of GCC economies.

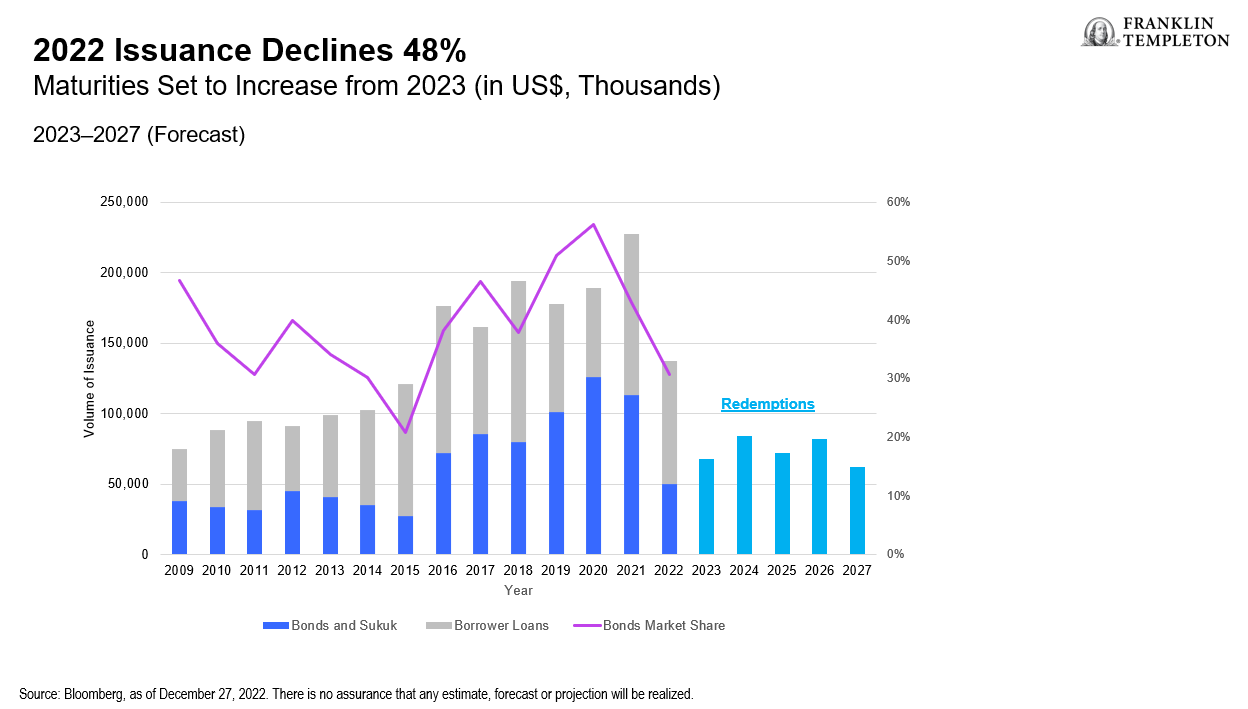

From a technical perspective, bond and sukuk issuance was down approximately 48% from a year ago,5 with demand stable or arguably increasing as foreign investors gradually reduced their structural underweight to the GCC. This last point is important. The GCC represents over 20% of the JPM EMBI Global Diversified Index and over 10% of JPM CEMBI Index, which we believe requires a thoughtful, active approach to regional allocations.

This explains much of the past, but where do we go from here?

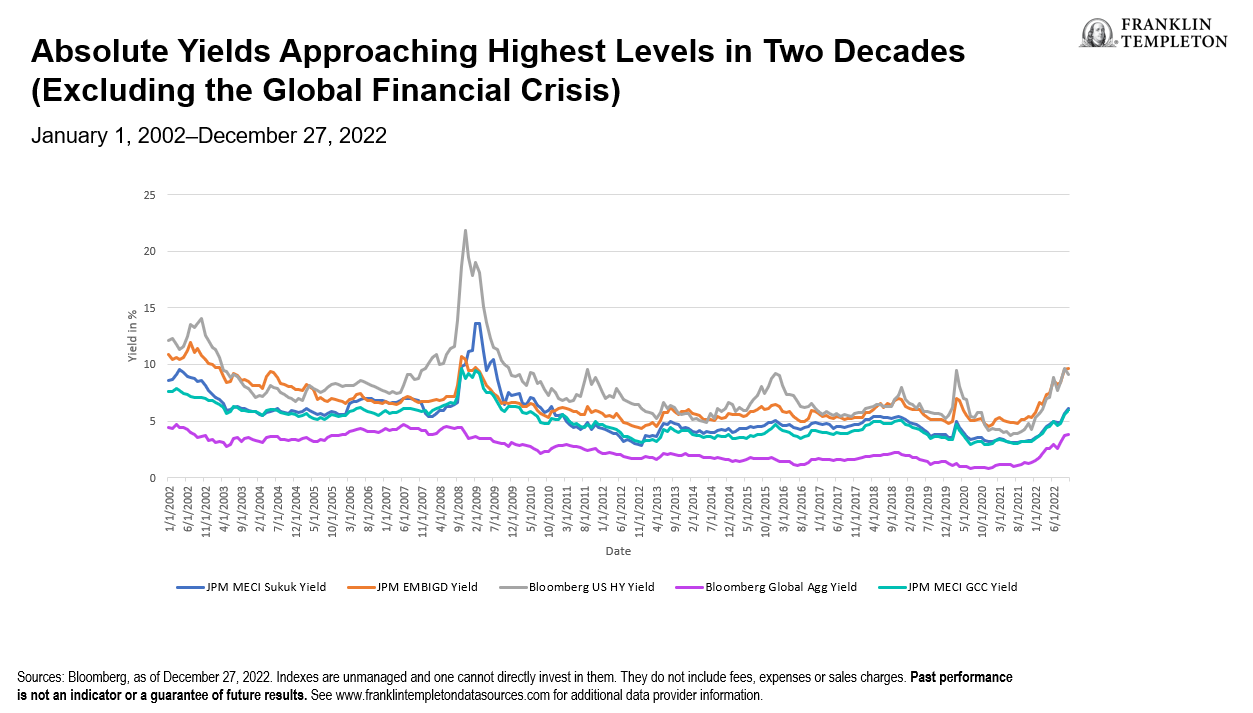

When we came into 2022, we expected the US Federal Reserve (Fed) to raise real rates and tighten financial conditions. By the middle of the year, we thought the job may have been done, with 10-year Treasury real rates above 0.75%, having moved from negative 1%.6 Real rates kept rising to above 1.5%, presenting attractive opportunities to take advantage of yields that had reached levels we have not seen in two decades. In a relatively short period of time, the Fed raised rates by 425 basis points, transforming the potential income production and protection fixed income can provide portfolios.

Looking into 2023, we believe investors will want to take advantage of these yields. The turnaround in fixed income may have already started in November, but the outlook for bonds and sukuk remain more attractive to us than other risk assets—certainly on a risk-adjusted basis, but potentially also on an absolute basis.

Exhibit 3: Historical Average Index Yield to Maturity in Percent

The challenge of course is that the Fed seems intent on continuing to tighten financial conditions, against what we see as an ongoing economic slowdown. We believe the Fed is guiding to a higher terminal rate well above 5%,7 intends to stay there at least through 2023, and only cut rates gradually thereafter.

The market may change its view as economic data comes through—particularly inflation data—but for now has lowered its estimate for the terminal rate slightly to 4.9% by March 2023, and expects rate cuts to begin by July 2023.

Implicit in both projections is that inflation has peaked, and the majority of rate hikes are behind us. From our perspective, it seems sensible to at least project stable benchmark rates, that may also decline faster if the recession in the United States is more significant, or inflation declines more rapidly. We recognize these as critical inputs and enter the year long duration.

Credit spreads are more challenging to forecast; there is a risk they widen. That is why we have a pronounced preference for higher-quality credits that have financial buffers to manage slowing economic activity. This is not to say we are not taking any risk, as there are opportunities in emerging markets that reflect dire outcomes that we think may not materialize, or at least compensate us for the risks involved. On average, however, our portfolios do have higher credit quality than the recent past.

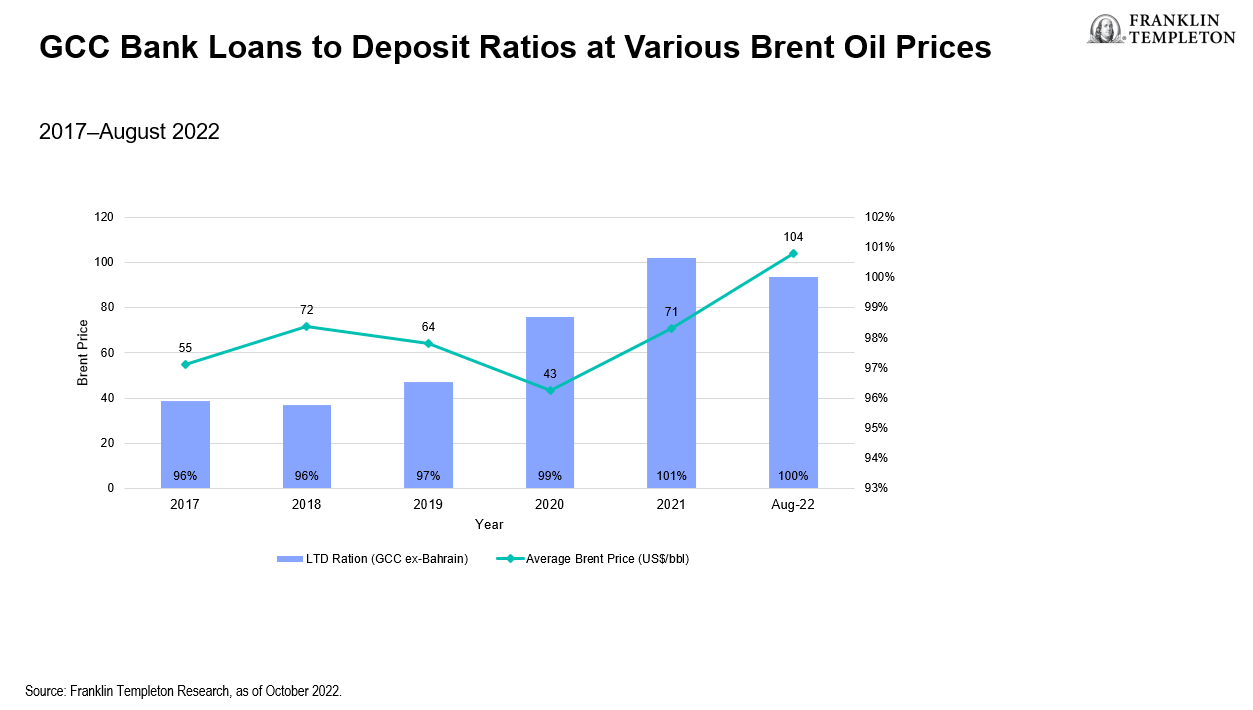

Oil may be vulnerable to slowing demand, but we think both OPEC+, through production cuts, and the US administration, through commitments to replenish its strategic petroleum reserves (SPR), should manage to keep oil prices above US$70 a barrel, which is enough to keep pressure on GCC credit trajectories at a modest level. It is worth considering that this oil-price cycle, because of reforms to national oil companies and fiscal budgets, has had a more benign impact on local liquidity, so financial conditions will likely remain tight across the GCC without further domestic monetary intervention.

Exhibit 4: GCC Banks’ Liquidity Measured Using Loans-to-Deposit Ratios (2017-August 2022)

The outlook for issuance appears set to improve, returning to annual levels of US$75-$80 billion on average. GCC governments are expected to see US$199.3 billion in fixed income maturities over the next five years (2023-2027), with corporate maturities at US$169.1 billion, for a total of US$368.4 billion).8 Saudi Arabia is expected to see maturities of US$125 billion until 2027, followed by UAE and Qatari issuers at US$109.8 billion and US$73.1 billion, respectively.9 The GCC’s share of emerging market issuance is set to increase, especially if lower rated (single B and below) issuers continue to struggle accessing primary markets.

Exhibit 5: GCC Bonds, Loans and Sukuk Issuance and Projected Bond Redemptions

After every sharp drawdown in fixed income, there have been strong recoveries. Though one must be careful not to discount the adjustment that bond markets have just lived through, we believe high-quality bonds have the potential to deliver the best risk-adjusted returns.

Faced with continued uncertainty and an abundance of risk, one may be tempted to time the market or wait for attractive entry levels. We believe this may be a mistake. In our view, it would be more prudent to focus on asset allocation and consider an increase in higher-quality fixed income sectors, including GCC bonds or global sukuk, that look poised to better defend portfolios and provide attractive levels of income.

WHAT ARE THE RISKS?

All investments involve risks, including the possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Investments in lower-rated bonds include higher risk of default and loss of principal. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value. In general, an investor is paid a higher yield to assume a greater degree of credit risk. The risks associated with higher-yielding, lower-rated debt securities include higher risk of default and loss of principal. Treasuries, if held to maturity, offer a fixed rate of return and fixed principal value; their interest payments and principal are guaranteed. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

___________________________

1. The Gulf Cooperation Council (GCC) is a political and economic union of Arab states bordering the Persian Gulf. Established in 1981, its six members are the United Arab Emirates, Saudi Arabia, Qatar, Oman, Kuwait and Bahrain.

2. The Dow Jones Sukuk Total Return Index is designed to track the performance of global Islamic fixed income securities, known as sukuk. The index measures an investment (excluding reinvestment) in US dollar-denominated, investment-grade sukuk that have been screened for Shariah compliance. The JP Morgan EMBI Global Index measures total returns for traded foreign debt instruments in emerging countries. The FTSE MENA Broad Bond Index tracks GCC corporate and sovereign bonds. The Bloomberg Global High Yield Index measures the global high yield debt market, representing the US High Yield, the Pan-European High Yield, and Emerging Markets Hard Currency High Yield Indexes. The Bloomberg Global Aggregate Index measures global investment-grade debt from 28 local currency markets including treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results. See www.franklintempletondatasources.com for additional data provider information.

3. Spreads are measured in basis points. The JP Morgan Middle East Composite Index (MECI) measures the performance of Middle East corporate and sovereign bonds. The J.P. Morgan Emerging Market Bond Index Global Diversified Index (EMBIGD) is a uniquely weighted USD-denominated emerging markets sovereign index. The Dow Jones Sukuk Total Return Index is designed to track the performance of global Islamic fixed income securities, known as sukuk. The index measures an investment (excluding reinvestment) in US dollar-denominated, investment-grade sukuk that have been screened for Shariah compliance. The J.P. Morgan Emerging Markets Bond Index Global (“EMBI Global”) tracks total returns for traded external debt instruments in emerging markets.

4. Source: IMF, COVID-19 Policy Tracker and staff calculations.

5. Source: Bloomberg, as of December 27, 2022.

6. Source: Bloomberg.

7 FOMC “Dot Plots” as of December 14, 2022, show a median of 5.125%, and a high of 5.625%. There is no assurance that any estimate, forecast or projection will be realized.

8. Sources: Bloomberg, Kamco Invest Research, GCC Fixed Income Market Update, December 2022.

9. Ibid.