Even amid still-elevated (though moderating) inflation levels, some economists offered cautiously optimistic global growth forecasts during last month’s World Economic Forum (WEF).

For starters, investors have eagerly anticipated China’s return. The country’s reopening—however bumpy—has lessened some market fears and led its currency to rally. From November (when China began to ease its strict COVID rules) through the end of January, the renminbi rose more than 7%, boosting market performance. Quarter-to-date for 2023, the FTSE China Index has climbed about 11%.1

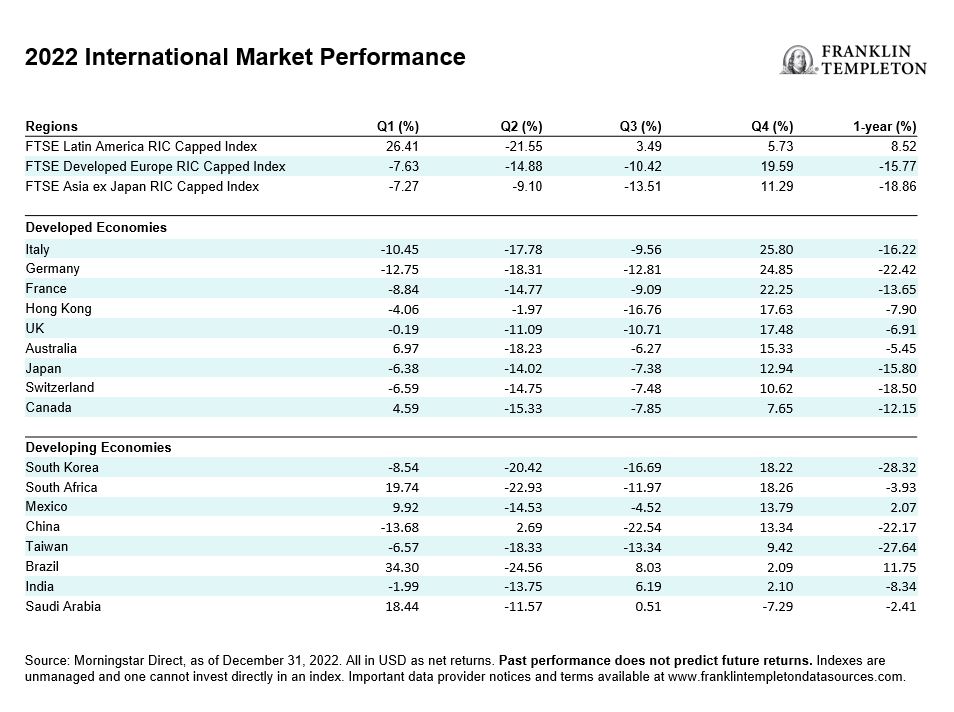

A wide divergence in single-country markets is already evident and comes on the heels of a year in which we saw a 40% delta between top-performing Brazil (+11.8%) and laggard South Korea (-28.3%). Fresh off this year’s starting blocks, Mexico led global equity markets. Heavily weighted toward consumer staples and financials, the FTSE Mexico Index climbed more than 16% in January.2 On the opposite end of the spectrum, recent turmoil facing Indian equities has led its market to slip -4%.3

Overall, however, investor appetite for emerging market equities remains strong, due to what we believe are attractive valuations and the likelihood of local currency appreciation to help boost international stocks.

China warrants a closer look

While global growth may still be dampened, China’s reopening marks a notable turning point. Given that it trailed significantly last year, we now expect pent-up savings and demand from Chinese consumers to further the country’s growth prospects, even if developed markets face a potentially mild recession. The government’s recent policy pivot away from pandemic restrictions led to the first surge in domestic travel in three years as well as large-scale Chinese New Year celebrations.

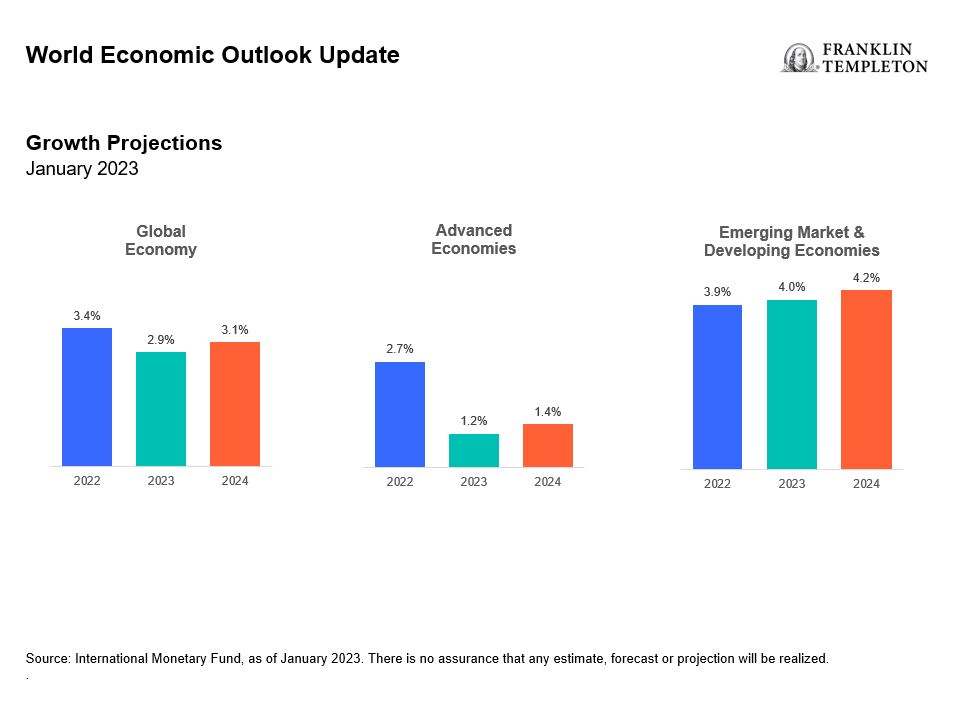

In its latest economic update, the International Monetary Fund (IMF) echoed sentiments from Davos, remarking that China’s reopening has “paved the way for a faster-than-expected recovery.” China’s economic growth is projected at 5.2% for the year, versus US growth expectations of 1.4%. The report also forecasts global growth of 2.9% for 2023, slightly higher than the IMF’s October forecast, and notes oil price spikes have not taken shape recently and labor markets remain fairly robust.4

Investors are now largely focusing on a developing market rebound. By some estimates, emerging market economies on average are expected to expand by about 3%-4% this year, outpacing developed market growth. There is some consensus that inflation will further recede as supply chain pressures lift, and investors will take the opportunity this year to pivot back toward undervalued emerging economies.

Taiwan and South Korea

While China grapples with more sustainable COVID-management policies and emerges from a trough, we’re likely to see a spillover effect for its major Asian trading partners, such as Taiwan and South Korea. These are two export-driven economies tied to the cyclical fortunes of semiconductor production. Chips markets suffered deep declines last year and appear ready for the tide to turn.

As trading resumed following the lunar new year holiday, investors piled back in. Taiwan’s stock market rose about 6% in US dollar terms, led by technology sector gains, from January 30 to February 3.5

Sensitive to fluctuations in global commodity pricing, South Korean markets struggled last year, but ended with a rally of more than 18% for the fourth quarter.6 Over the long term, cutting-edge Korean firms that lead in industries such as autos, electric vehicle (EV) batteries and memory chips appear competitively positioned for growth.

Mexico

In our view, Mexico is another economy well positioned to benefit from reconfigurations in global supply chains as many multinationals diversify away from China. Its gross domestic product (GDP) expanded 0.4% in the fourth quarter from the prior three months.7 And in January, the IMF raised its forecast for the country’s 2023 GDP growth to 1.7% from 1.2%.8

Increasingly, global manufacturers are investing more aggressively in Mexico as part of a wider trend known as “near-shoring,” which allows production to be closer to key trading partners. This has likely helped Mexico’s labor force. Notably, Mexico reached a lower-than-expected jobless rate of 2.8% in December, versus the 3.5% seen in December 2021. Remittances (funds sent from citizens working abroad) have also soared in recent years.9

As the global maritime sector continues to pursue ambitious decarbonization goals, Mexico holds significant advantages for a “robust zero-carbon shipping fuels” industry, according to the WEF. Research studies published last year reveal expectations that the country’s abundant supply of renewables can position Mexico as a leading exporter of clean fuels, which will not only fast-track Mexico’s transition to a low-carbon economy but also be a boon for new green jobs.10

At the end of last year, Mexico’s equity market, as measured by the FTSE Mexico RIC Capped Index, increased 2% on an annualized basis following its fourth-quarter rally of nearly 14%.11 Inflation, however, remains stubbornly high in Mexico despite early and aggressive intervention across central banks in Latin America last year. But analysts continue to expect inflation to slow in 2023 and remain below the September peak.

For those implementing global asset allocation, we often tout the benefits of single-country and regional ETFs as tools that can help investors create differentiated outcomes. In our opinion, selecting cost-effective investment vehicles, such as single-country ETFs that are tailored for precise implementation, can make sense in this environment for many investors.

We believe investors should think about country allocation with the following considerations:

- Fundamentals: the companies and sectors that represent each country

- Macroeconomic: GDP growth, monetary policy, geopolitical, demographics

- Emerging themes: more transient trends that favor select countries

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in developing markets involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. China may be subject to considerable degrees of economic, political and social instability. Investments in securities of Chinese issuers involve risks that are specific to China, including certain legal, regulatory, political and economic risks.

ETFs trade like stocks, fluctuate in market value and may trade above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns. ETF shares may be bought or sold throughout the day at their market price on the exchange on which they are listed. However, there can be no guarantee that an active trading market for ETF shares will be developed or maintained or that their listing will continue or remain unchanged. While the shares of ETFs are tradable on secondary markets, they may not readily trade in all market conditions and may trade at significant discounts in periods of market stress.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

__________

1. Source: Bloomberg, as of February 3, 2023. Past performance does not predict future returns. Indexes are unmanaged and one cannot invest directly in an index. Important data provider notices and terms available at www.franklintempletondatasources.com.

2. Ibid.

3. Ibid.

4. Source: IMF, “World Economic Outlook,” January 30, 2023. There is no assurance that any estimate, forecast or projection will be realized.

5. Source: Bloomberg.

6. Source: Morningstar Direct, as of December 31, 2022.

7. Source: Bloomberg, January 31, 2023.

8. Source: IMF, “Mexico,” November 4, 2022.

9. Source: IMF, “The Unexpected Rise in Remittances to Central America and Mexico During the Pandemic,” September 21, 2022.

10. Source: WEF, “Why Mexico is ideally placed to become a zero-carbon shipping fuels hub,” February 7, 2022.

11. Source: Morningstar Direct, as of December 31, 2022.