The Middle East and North Africa (MENA) region is benefiting from a resurgence in growth. Giga-investment projects, elevated energy prices, greater fiscal responsibility, and improving demographics are among the drivers. An additional tailwind for equity investors is the increasing weight of MENA in emerging market equity indexes.

MENA stock valuations, as measured by price-to-earnings ratios, have declined from their March 2022 peak, and now sit comfortably below their 10-year average of 13.5x.1Earnings growth in the region is forecast to increase by mid-single digits in 2023, driven by rising investment and consumption.2

This combination of lower valuations and positive earnings growth potential has led our on-the-ground research team to uncover company-specific investment opportunities in sectors that hitherto did not fit our investment criteria.

Giga investment projects

The Gulf Cooperation Council (GCC)3 has big spending plans, especially in Saudi Arabia, the region’s largest economy. As part of its Vision 2030 economic transformation plan, the government has announced its intention to invest over US$2 trillion in the domestic economy between now and the end of this decade.

Giga-projects have been the cornerstone of the multi-year reform process underway in the region. The imperatives of diversifying the economy away from oil, attracting capital and talent, and generating jobs for a young population have driven sustained momentum on the projects despite local and global headwinds.

The steady progress on giga-projects despite the volatility in oil prices and the COVID-19 pandemic reflects the government’s long-term commitment. By mandating the country’s sovereign wealth fund as the independent sponsor of these projects with its own balance sheet, the government has endeavored to separate the outcomes of the projects from fluctuations in their fiscal position and, by extension, oil prices. This is a major departure from the past when government spending was tightly linked to oil prices.

In Dubai, its economic Agenda 2033 aims to double the size of economy and place the city among the top three economic cities in the world. Dubai will focus on foreign trade, foreign direct investment, private sector investments, and government spending to achieve its 2033 goals.

In the energy space, Qatar plans to increase its liquefied natural gas (LNG) capacity to 110 million tons per year by 2026.4 Qatar will provide Germany with LNG under a long-term supply deal reflecting Germany’s efforts to wean itself off Russian gas.

Energy price outlook

We remain bullish on the energy price outlook over the medium-term. In our view, the balance of risks for oil prices in 2023 appears to be on the upside, given the reopening of China, a continued revival in global travel, and the embargo/price cap on Russian oil by the United States and the European Union.

Greater fiscal responsibility

The four major countries in the GCC (Saudi Arabia, the United Arab Emirates, Qatar, and Kuwait) are expected to experience double surpluses due to elevated oil prices, on both their fiscal and current accounts.

Fiscal surpluses during 2022 didn’t translate into excessive government expenditure, which has been a common policy approach of the GCC nations during times of excess in the past. This time around, the GCC governments have acted prudently and focused on their long-term economic agendas rather than provide a short-lived stimulus. transferring capital to state sovereign wealth funds.

Improving demographics

In a world grappling with the challenges of falling birth rates and increasing dependency ratios, the demography of the GCC economies, particularly Saudi Arabia, is moving in the opposite direction. Rising birth rates, a falling dependency ratio, and social reforms are powerful combinations which have the potential to raise the potential growth rate of GCC economies.

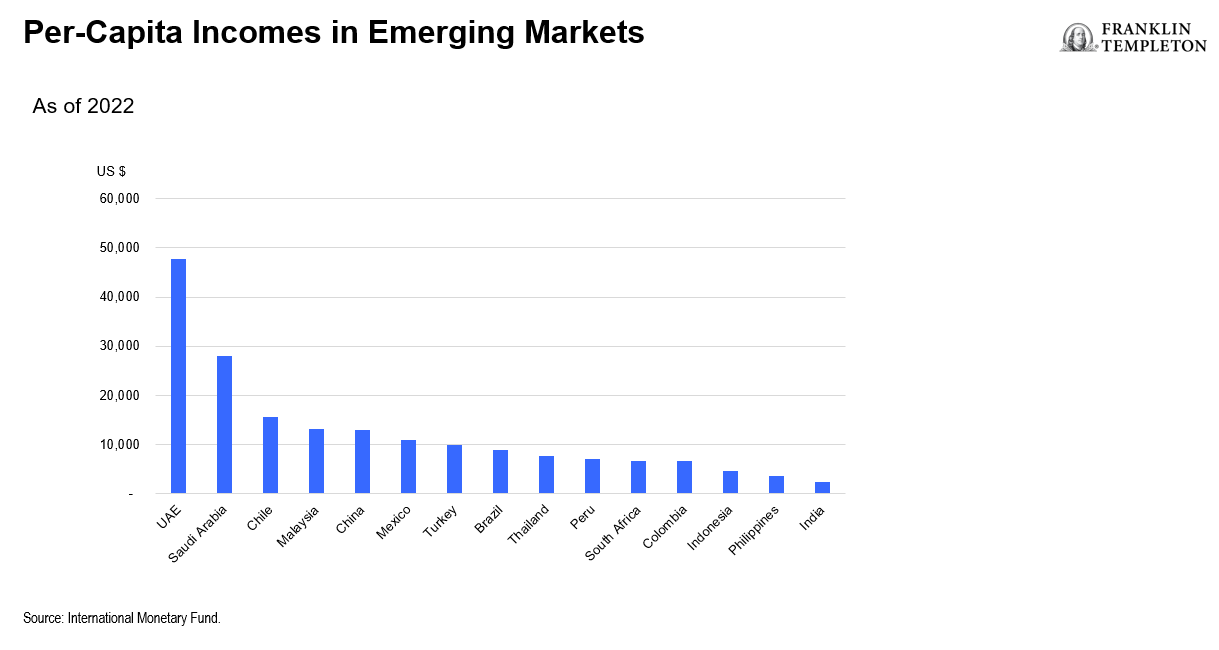

Saudi Arabia is currently in the demographic sweet spot, with high and relatively stable births, and low and stable deaths. Saudi Arabia’s expected growth in the economically active 25-64 year old population is among the fastest in emerging markets: 19.6% between 2019-2039, only the Philippines 43% growth rate is higher.5 In our view, positive demographics in Saudi Arabia, combined with high per-capita income (US$28,000) and political stability provides a tailwind for consumption, and in turn economic growth.6

MENA’s rising weight

MENA’s weight in the MSCI Emerging Markets Index has increased from 1.6% in 2016 to 7.7%, as of 2022.7 The implementation of several market-based reforms in recent years has driven this increase. These include initial public offerings, privatization and increasing foreign ownership limits. Saudi Arabia is the largest single market, with a weight of 4.1% in the Index—which looks likely to increase.

A positive backdrop

In sum, we see a positive backdrop for MENA equity markets in 2023. The region is not immune from risk, including the impact of rising interest rates on growth and, in turn, the demand for energy, as well as the impact of Russia’s war in Ukraine. Nevertheless, the connection between oil prices and the economic and market outlook for MENA is being steadily diluted thanks to economic diversification and a greater reliance on sovereign wealth funds to finance investment in the region.

WHAT ARE THE RISKS?

All investments involve risks, including the possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

________________________

1. Source: Bloomberg, as of December 31, 2022.

2. Source: Bloomberg, as of December 31, 2023.

3. The GCC is a political and economic union of Arab states bordering the Persian Gulf. Established in 1981, its six members are the United Arab Emirates, Saudi Arabia, Qatar, Oman, Kuwait and Bahrain.

4. Source: Reuters. “Qatar’s LNG production capacity to reach 126 mln T a year by 2027, says Emir.” February 2022, 2023.

5. Source: UN World Population Prospects, 2022.

6. Source: IMF World Economic Outlook, January 2023.

7. Source: MSCI. Indexes are unmanaged and one cannot invest in them. They do not include fees, expenses or sales charges. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. See www.Franklintempletondatasources.com for additional data provider information.