Three things we are thinking about today:

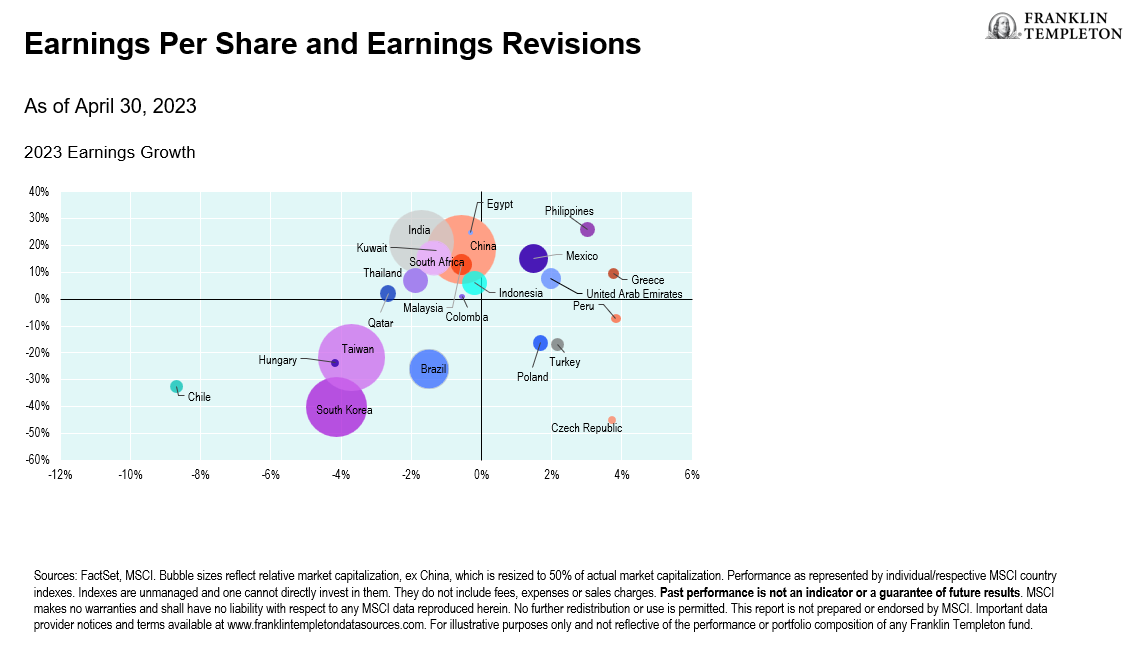

- Earnings season. The earnings season in emerging markets is underway. Flat headline earnings growth in 2023 masks significant divergence across individual markets. Consensus expectations for China is for earnings growth of 20%, with India also expected to witness double-digit growth.1 However, heavyweight markets in Taiwan and South Korea are expected to witness a contraction in earnings of 26% and 40% respectively. This is primarily due to weakness in the semiconductor sector, which has a large weight in both markets. Commodity-heavy markets—including Brazil and Saudi Arabia—are also forecast to witness a contraction in earnings due to lower commodity prices compared to the year-earlier period.

- Rising resource nationalism. The Chilean government is issuing new rules on lithium mining in the country. Future projects are required to have the state as the majority shareholder. The goal of the policy is to raise output to meet the forecast increase in demand for lithium, which is a key input to electric vehicle battery production. The government has indicated it will honor existing mine concessions, which for the largest projects expire in 2030 and 2047. There are lingering concerns about how the government will execute the policy and the impact on future contract negotiations. The decision to impose the state as the largest shareholder in future projects reflects a global trend toward government tightening controls over strategic industries.

- A tale of two sectors. Recent purchasing manager index (PMI) data highlight divergent trends in the services and manufacturing sectors across emerging markets (EMs). Services-sector PMI is firmly in expansionary territory in China and Brazil, whereas manufacturing PMI data in the same economies have weakened in recent months. This trend reflects the post-COVID pivot toward services, and concurrent dip in demand for manufactured goods. This has negative implications for EM economic growth, as manufacturing tends to have a higher weight in these economies relative to services. Conversely, it has potentially positive implications for equity markets as the weight of broadly defined services is larger than the weight of broadly defined manufacturing in EM equity indexes.

Outlook

While inflationary worries continue to dominate the headlines, we remain steadfast in our view that inflationary pressures are more muted in EMs compared to developed markets. Within EMs, we are already seeing signs of slowing inflation growth in markets including Brazil, China, India and South Korea.

In addition to the swift tightening of monetary policy when signs of inflation first emerged, EM economies’ targeted measures to control inflation have finally borne fruit. Some measures EMs have adopted include: financial assistance directed toward vulnerable groups instead of broad-based payouts; a commitment to securing investments through reforms and funding; and reducing tariffs.

Given the slow decline in inflation, our portfolios are still positioned to cushion the impact of an inflationary environment. Our focus on company fundamentals and a preference for businesses with sustainable earnings trading at a discount to their intrinsic worth favors companies which are leaders in their respective fields and that enjoy greater pricing power amid higher inflation. Our focus on quality, near-term cash flows and returns to shareholders is also beneficial when longer-duration sources of growth—the future income streams of high growth stocks—are sharply discounted due to rising interest rates, which are often a side effect of inflation.

Our bottom-up focus gives rise to a portfolio that is characterized by a high active share and exposure to off-benchmark holdings. This is due to the local expertise our on-the-ground teams garner. The timely insight from company management, business leaders, suppliers and consumers is the foundation of our focus on company fundamentals, which allows us to position our portfolios for the longer term.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with investing in foreign securities, including risks associated with political and economic developments, trading practices, availability of information, limited markets and currency exchange rate fluctuations and policies; investments in emerging markets involve heightened risks related to the same factors. Investments in fast-growing industries like the technology and health care sectors (which have historically been volatile) could result in increased price fluctuation, especially over the short term, due to the rapid pace of product change and development and changes in government regulation of companies emphasizing scientific or technological advancement or regulatory approval for new drugs and medical instruments. China may be subject to considerable degrees of economic, political and social instability. Investments in securities of Chinese issuers involve risks that are specific to China, including certain legal, regulatory, political and economic risks.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

__________

1. There is no assurance that any estimate, forecast or projection will be realized.