In my previous article on “China’s consumption triangle—a possible trinity,” I mentioned that China’s domestic consumption is the biggest upside opportunity in the next six to 12 months. Many will disagree with me as recent macro data has revealed a post-COVID reopening recovery that has been bumpier than expected. Consumer confidence has been patchy, while the services sector recovery has been more encouraging. Such circumstances have led policymakers to tread carefully. However, there are increasing signs that more stimulus measures are getting underway. Multiple government agencies are drafting these measures and it was reported that the State Council will discuss these policies very soon. They will likely include at least a dozen measures designed to support real estate and domestic demand. The Chinese authorities are gaining confidence that they can unleash a bull in the “China shop” without breaking the porcelain.

Did you know?

Apparently, the idiom “bull in a china shop” was already in use in the 1800s as a title of a song in a pamphlet printed by M. Angus and Son, circa 1800. However, many had theorized that the idiom may have originated in the 17th century in London when somebody brought cattle to the market. Presumably, some bulls managed to escape and got inside a crockery shop. Thus, the idiom was born. It has of course evolved to describe the scenario where a big animal knocking down the delicate crockery (also known as china) from the shelves in a shop, leaving a mess. French, German and a few other European languages have a similar idiom. Curiously, according to some other stories, it wasn’t a bull that got into the china or porcelain shop, but an elephant. After all, a male elephant is also known as a bull. Interestingly enough, a few years ago the TV show MythBusters put “bull in a china shop” to the test. They showed not one but several bulls running around a makeshift china shop. Surprisingly, not one bull broke a single dish. The bulls were running, but they were nimble enough to avoid the shelves. Maybe the French and the Germans were right. It was the elephant that behaves like a, well, bull in a china shop.

Here are my latest observations:

In short, over the past six months China’s reopening has not delivered the growth that President Xi Jinping and his government favor, and so policy is beginning to shift. As reported in the media, China is mulling a new property-market support package and regulators are considering a new basket of measures, including reducing down payments in some non-core areas of key cities, further relaxing purchase restrictions, as well as refining and extending policies announced in the “16 financial measures” from November 2022.1 In addition, media reports indicate that the Chinese authorities are guiding big banks to lower deposit rates by 10 basis points (bps).2 That preceded the People’s Bank of China’s announcement of a 10 bps cut in the seven-day repurchase rate from 2%.3 The move may be small, but it conveys their intent to boost growth. Finally, the State Council recently reiterated its commitment to support the production and adoption of electric vehicles (EVs) through extending the purchase tax reduction and promoting the construction of high-quality charging infrastructure.

Additionally, fiscal policy will be eased in a targeted and measured fashion. Beijing understands that government support is required to stem an erosion of domestic confidence in the recovery. Local and foreign investors are closely watching policy responses as the government makes decisions crucial for China’s medium-term growth and wealth creation.

Finally, investors should also note changes at the regional level, above all at the six “economically strong provinces.” These six provinces account for about 45% of national gross domestic product (GDP)4 and make up nearly 60% of the national total for foreign trade.5 They include the coastal, export-heavy provinces of Guangdong, Jiangsu, Zhejiang and Shandong, as well as the landlocked provinces of Henan and Sichuan. These provinces have their 2023 GDP growth target at 5%-6%.6 Investors, in other words, should look beyond Beijing and Shanghai.

Bears have a point, but bearishness is overdone

Those in the bearish camp are flagging deflation risks, record high youth unemployment, scant signs of foreign direct investment (FDI) recovery, and elevated US-China tensions that are hindering bilateral trade and cross-border investment flows.

Some foreign investors are now questioning China’s role as a contributor to global economic growth. Those concerns appear exaggerated, in our opinion. True, between 2013 and 2021 China’s average contribution to global economic growth exceeded 30%, ranking first across the world, a level that probably cannot be sustained.7 But in doing so, China leapfrogged to a large economy and a major force in world GDP. By 2021 China’s GDP accounted for 18% of world output, up from 11% in 2012.8 China’s real GDP expanded at an average annual growth rate of 6.6% percent from 2013 to 2021 versus 3.0% for the global economy and 4.1% for developing economies.9

The bottom line is that the well-being of China will play a vital role in the prosperity of the rest of the world. China’s growth during global dislocations this century has cushioned other economies from shocks. Concerns about China’s diminishing role as the global pillar are misplaced. If anything, China is slated to become an even larger contributor to the world economy, passing a fifth of global output in the coming five years. Even rising trade protectionism, which has halved China’s exports (as a % of GDP) from its peak at 40% in 2006, has not hampered China’s contribution to global growth nor its emergence as one of the world’s most powerful economic blocs (alongside the European Union and the United States).10

What does this mean for Chinese investments?

Thus far in 2023, Chinese equities have been lagging behind not only US markets, but also versus Japanese and German indexes.11 Weaker-than-expected China growth has been a clear drag on mainland share price performance, as have been significant downward revisions in corporate profits.12 The Chinese equity market has derated this year.13

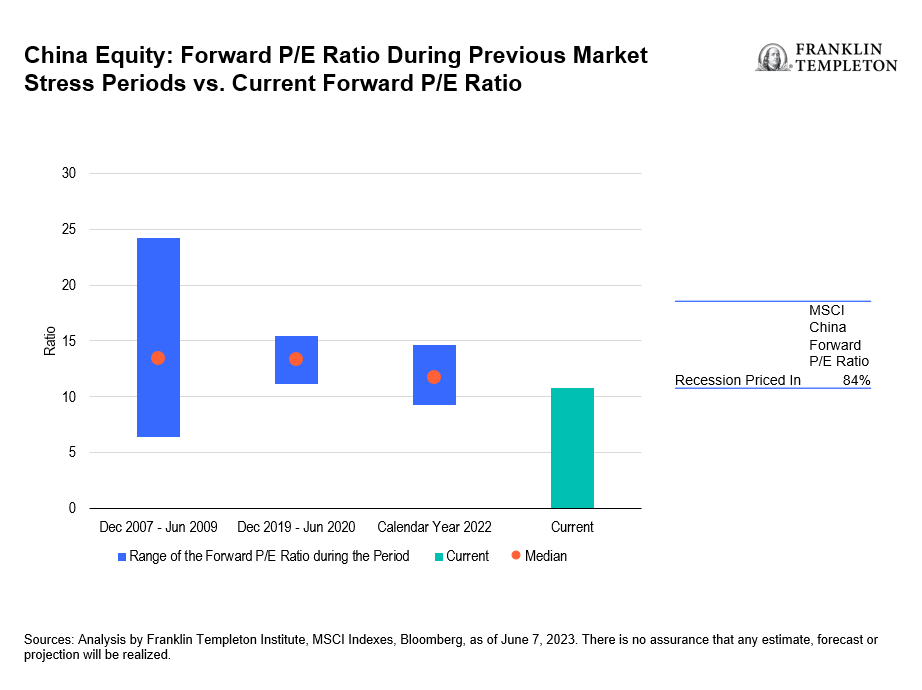

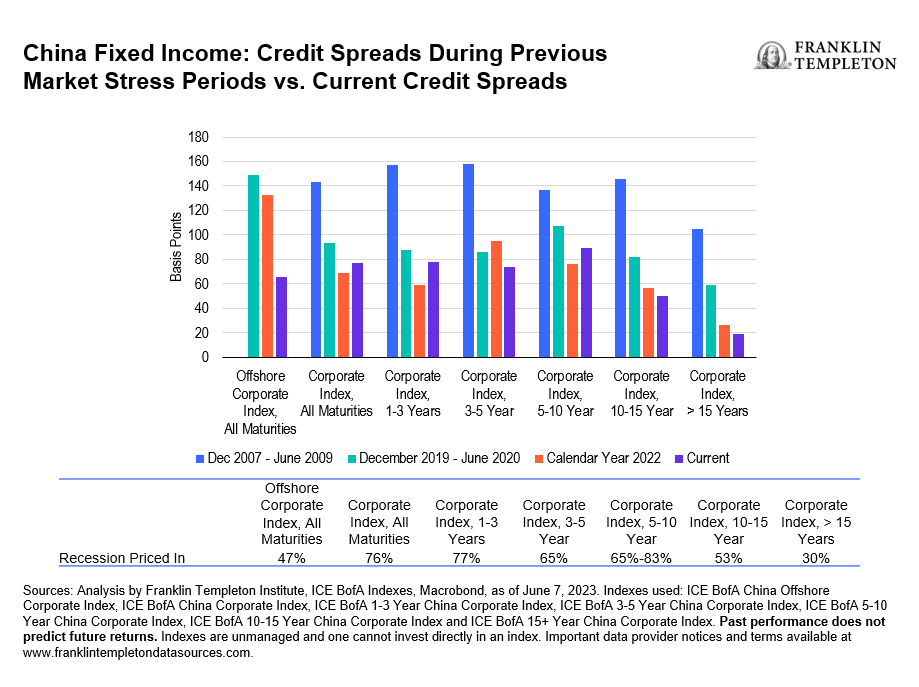

But as a consequence, Chinese stocks have also already factored in a lot of bad news. For instance, based on our calculation, the Chinese equity market now discounts more than an 80% probability of recession. That probability is based on the MSCI China Index forward price-to-earnings (P/E) ratio of 10.8x, which is now below the median ratios of previous market stress periods, including the global financial crisis (13.4x), the COVID-19 pandemic (13.3x) and 2022 (11.7x).14 Similarly, the Chinese credit markets are pricing in recessionary risks, reflected in the wide credit spreads in the one-three years and five-10 years maturity ranges.15

With a fair amount of negative news already priced in as well as the pending policy stimulus, we anticipate a 2023 second-half recovery for Chinese markets. The recovery is likely to happen in stages.

It is worth recalling that optimism about COVID reopening at the end of last year led to foreign portfolio inflows worth US$25 billion in the first five months of 2023.16 But interest waned as the economy stuttered, triggering outflows of US$2.4 billion in April and May.17 As policy becomes more supportive, we expect renewed interest in the market as growth and profits expectations turn up and against the backdrop of what we consider attractive valuations.

Equity investment opportunities are apt to tilt toward manufacturing, especially in industrial equipment, and in the banking sector. In our analysis, industrial equipment should benefit from a probable rise in capital expenditure as the economy improves. For banking, we believe stable earnings and strong asset quality accompanied by attractive valuations are key supports.

Finally, we would be remiss if we did not note that the global economic outlook is also improving. Signs of falling inflation without sharp economic slowdowns in the United States or in Europe are bolstering global investor sentiment. Policy rates are nearing their peak in the United States, with Europe not far behind. In our opinion, the global profits recession appears to have bottomed, with upward revisions now the norm in most regions.

We believe China and Chinese equities will likely benefit from these developments. It is becoming increasingly evident to us that the narrow base of equity leadership, which dominated market performance in the first half of 2023, is giving way to greater global participation. With China at the nadir of its business and profits cycle, but also offering what we consider compelling valuations, it is well poised to join the broadening global equity market recovery that could be a hallmark of the second half of 2023.

Conclusions: Do not fear the bull in the china shop

The “bull in a china shop” tends to be associated with fragility of the surroundings and the presence of clumsiness.

But that is not the same as being an equity bull in the shop that is the Chinese equity market. We believe that appropriate policy support—coordinated between the central and regional governments—should make the disappointments of China’s recovery that have plagued its equity market thus far this year a thing of the past. An improving global outlook is also supportive, as is a growing willingness of investors to broaden their horizons.

In this sense, we welcome the bull in the China shop. There is value to be found in traipsing around its assets.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

The government’s participation in the economy is still high and, therefore, investments in China will be subject to larger regulatory risk levels compared to many other countries.

There are special risks associated with investments in China, Hong Kong and Taiwan, including less liquidity, expropriation, confiscatory taxation, international trade tensions, nationalization, and exchange control regulations and rapid inflation, all of which can negatively impact the fund. Investments in Taiwan could be adversely affected by its political and economic relationship with China.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

__________

1. Source: Bloomberg, “China Asks Big Banks to Cut Deposit Rates to Boost Growth,” June 6, 2023.

2. Source: Bloomberg, “China’s Surprise Rate Cut Fuels Expectations of More Easing,” dated June 13, 2023.

3. Sources: China Customs Statistics Information Center, Macrobond, as of March 31, 2023.

4. Sources: Analysis by Franklin Templeton Institute, National Bureau of Statistics, Bloomberg, as of 2022.

5. Sources: Analysis by Franklin Templeton Institute, National Bureau of Statistics, as of 2021.

6. Source: China Briefing, “China 2022 Economic Growth – A Breakdown of Provincial GDP Statistics,” February 6, 2023.

7. Source: National Bureau of Statistics Report, September 2022.

8. Source: IMF World Economic Outlook, April 2023.

9. Sources: Analysis by Franklin Templeton Institute, IMF World Economic Outlook (April 2023), Macrobond.

10. Sources: China Customs Statistics Information Center, Macrobond, as of March 31, 2023.

11. Source: Bloomberg, as of June 15, 2023. Indexes used are: United States – S&P 500 Index, Japan – Nikkei 225 Index, Germany – Deutsche Boerse AG German Stock Index, and China – Shanghai Stock Exchange Composite Index. Past performance does not predict future returns. Indexes are unmanaged and one cannot invest directly in an index. Important data provider notices and terms available at www.franklintempletondatasources.com.

12. Sources: Analysis by Franklin Templeton Institute, Shanghai Stock Exchange Composite Index, Bloomberg, as of June 15, 2023.

13. Sources: Shanghai Stock Exchange Composite Index, Bloomberg, as of June 15, 2023.

14. Sources: Analysis by Franklin Templeton Institute, MSCI Indexes, Bloomberg, as of June 7, 2023. There is no assurance that any estimate, forecast or projection will be realized.

15. Sources: Analysis by Franklin Templeton Institute, ICE BofA Indexes, Macrobond, as of June 7, 2023.

16. Source: Reuters, “Investors channel billions into emerging markets, but China drops again, IIF says,” June 9, 2023.

17. Ibid.