Key points

- The fifth-largest economy in the world appears to be facing an unprecedented window of opportunity. International investors are asking: Is this the new China?

- India is big, it has a young population, and the government has implemented various “business-friendly” reforms. But it is still classified as a “low-income country” by the World Bank. The investment case for India rests on the assumption that it will make the move to “upper middle income” relatively easily, implying it doubles its gross domestic product (GDP) per capita to over US$4,466.1

- Such a move would be exceptional and underlines the potential that India’s exciting technology, software and communications sectors present. The growth of the middle class has predictable positive impacts on all aspects of consumer, housing and related sectors.

- To realize these changes and unleash this potential, we believe India must deploy a combination of long-term-oriented policies to address structural constraints, and execute short-term, pragmatic infrastructure investments. The overriding principle should be to set the conditions to support growth, with a unified approach, covering employment, education, infrastructure investment, and climate change insulation.

- Trade is a big potential driver of economic growth and of employment. According to the World Trade Organization (WTO), which India joined in 1995, the average Most Favored Nation (MFN) applied import tariff India applied was 18.1% in 2022, the fourth-highest in the World Trade Organization (WTO), after Sudan (21%), Tunisia (19%) and Algeria (18.9%).2 For reference, the European Union is at 5.1% and the United States is at 3.3%. For agricultural imports, India’s equivalent tariff is 39.6%. The pace of development could be further accelerated, and broadened across more sectors, by membership of free trade agreements such as the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), which involve giving up domestic protection, but provide market access to 11 countries that represent 15.6% of world GDP. In our view, there is a window of opportunity for India to turbocharge its economic development and enable it to integrate meaningfully with the global trading system and “punch its geopolitical weight” in Asia and the world.

- India’s young demographics are usually presented as a positive, but the reality is more complex. Having a lot of young people is clearly good, but they need to be healthy enough to work and educated enough to learn appropriate skills for the labor market. India doesn’t need millions of Ph.D.s, but rather, a relatively well-educated pool of young people, because they are more easily employable. Given the trend toward automation and artificial intelligence (AI), the growth of the “knowledge” economy drives demand for skilled workers. A young, well-educated labor force will attract investment in high margin, productive areas, providing a positive driver for economic growth.

- The country’s climate change vulnerabilities and their potential impact on social structure are not particularly well-known. India uses over 90% of its fresh water on agriculture. 3 This is clearly inefficient, because the global average is 70%, but millions of farmers still depend on the monsoon rains, which have become less regular while heatwaves have become more frequent over the last 20 years. Meanwhile, the Indus, Brahmaputra and Ganges River basins are amongst the most water-stressed river basins in the world, according to a study by the European Commission.4 This is due to a combination of lower volumes of seasonal meltwater from the Hindu Kush Himalayan region due to the negative impact of climate change, the increasing populations in Pakistan, India and Bangladesh which strain existing water resource, and the threat of water diversion from China.

- Indian equity market valuations suggest that investors have high conviction in the likelihood of earnings growth, but also reflect the lower free floats, as the controllers/promoters of companies tend to maintain close to 50% ownership in public companies. Against that, middle-income households have only 10% of assets in mutual funds or capital market investments, implying a potential wave of domestic investors in future.5 Another relevant factor is that certain sectors in India, such as fast-moving consumer goods companies, deliver margins that are significantly wider than global averages. Meanwhile, the development of the domestic fixed income market bodes well for deeper financing availability for both government and corporates.

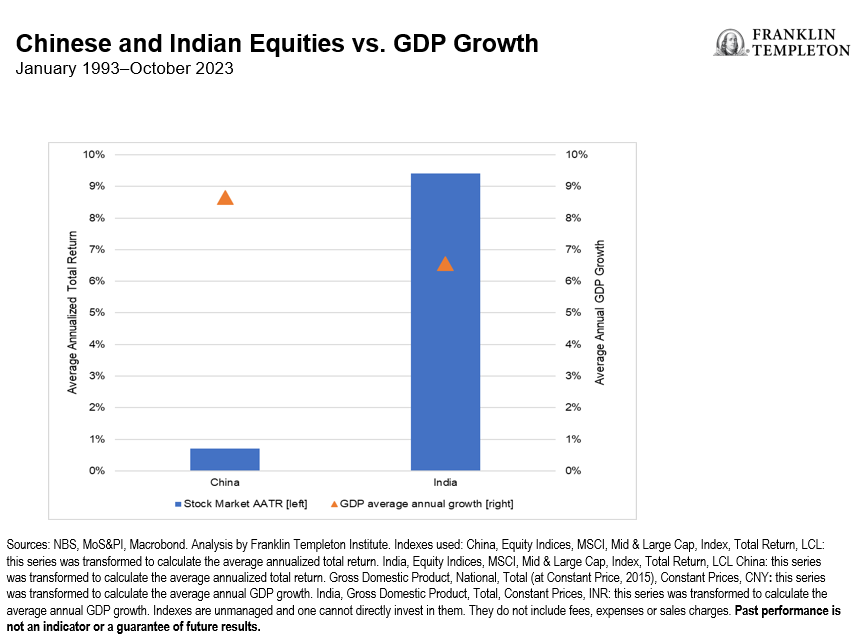

- Typically, international investors are drawn to fast-growing economies on the premise that these markets hold more promise for equity investors. However, experience suggests that it is unusual for equity returns to match nominal GDP growth over time. In the chart below, while Chinese GDP growth as averaged 8.65% per annum in the last 30 years, the equity market’s average total return has been +0.7%. By contrast, India has had GDP growth of 6.5% per annum, yet the equity market has delivered an average total return of 9.4% in the same period.6

GDP vs. Stock Market Returns Over 30 Years

- India remains an interesting place to invest, but in a more defined range of opportunity than in the past. For asset owners, we believe that India is not the new China. It is potentially a new India.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Investments in companies in a specific country or region may experience greater volatility than those that are more broadly diversified geographically.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

_________

1. Source: World Bank, Country Classifications by Income Level for 2024. June 30, 2023.

2. World trade Organization, (WTO) World tariff profiles 2023. Data as of 2022.

3. Source: Food and Agriculture Organization of the United Nations (FAO) Aquastat Database.

4. Source: “An innovative approach to the assessment of hydro-political risk: a spatially explicit, data driven indicator of hydro political issues—2018,” F. Farinosi, C. Giupponi, A. Reynaud, G. Ceccherini, C. Carmona-Moreno, A. De Roo, D. Gonzalez-Sanchez, G. Bidoglio. European Commission. As of June 2020.

5. Source: CRISISL. “The big shift in financialization.” December 2022.

6. Past performance is not an indicator or a guarantee of future results.