While Western season’s greetings are merry with wishes of joy, peace, love and blessings, those for Chinese cultures tend toward “good fortune.” In tandem with happiness for the Lunar New Year, wishes for prosperity are typical—and something that China investors could certainly use as we enter the year of the dragon.

China and Hong Kong markets had a humbling 2023 with equities down more than 10%. Fortunately, regulators in Beijing have turned up the dial on reform measures to stoke some of that auspicious dragon luck. Expectations are rising for even more support to come. In early February, China’s central bank made changes to allow its financial institutions to hold smaller cash reserves, cutting the reserve requirement ratio by 50 basis points. This is set to release nearly US$140 billion in long-term capital as Beijing seeks to boost targeted growth and market confidence.

A rise in the country’s passenger vehicle sales also offers some hope, and 2023 saw China surpass Japan as the world’s largest car exporter.1 Year-over-year retail passenger car sales were up 57% in January, according to the China Passenger Car Association. The country’s expertise in so-called new-energy vehicles—fully electric and plug-in hybrids—is partly responsible for the export surge.2 Another important shift to note is that China’s auto industry is increasingly shipping to wealthier countries—exports to Australia tripled year-over-year during the first half of last year and sales to Spain rose 17-fold to nearly 70,000 vehicles.3 With renewed government support, China’s electric vehicle (EV) makers are making a big splash on the world stage. Shenzhen-based automaker BYD overtook Tesla as the world’s top seller of EVs at the end of 2023, and China’s overall passenger EV sales are forecast to make up 59% of world sales this year, compared to 50% in 2019.4

Still re-opening

Beijing has also begun stepping up tourism and travel promotions, granting visa-free entry to 11 countries, with Singapore and Thailand the latest to be included. Other policies to combat soft consumer demand include simplified visa procedures that allow travelers to apply for entry permits upon arrival at some ports and lower visa application fees for some foreign nationals.

In our view, Beijing’s recent spate of new reform policies should hold long-term benefits for its state-owned enterprises (SOEs), including its “big four” banks, as well as corporations entrenched in the country’s energy sector. Of course, China’s domestic deflationary pressures and real estate market weakness remain dominant concerns.

Beyond the Magnificent Seven (Mag7),5 which drove US equity returns last year, the broader equity market had less impressive returns over the same period. Big tech’s outperformance, coupled with sharp declines in China, may have also obscured some encouraging trends for emerging markets (EM), where we saw pockets of stellar performance. Understandably, global investors may feel inclined to await more regulatory clarity before warming to China’s markets. Keep in mind that a typical EM portfolio, such as the FTSE Emerging Index, holds about a 25% weighting in mainland China versus 18% for Taiwan.6 The MSCI AC Asia ex Japan Index holds a 29% exposure to China versus 19% for Taiwan.7 So for a more precise, targeted approach, investors may consider low-cost single country-focused exchange-traded funds to express tactical views.

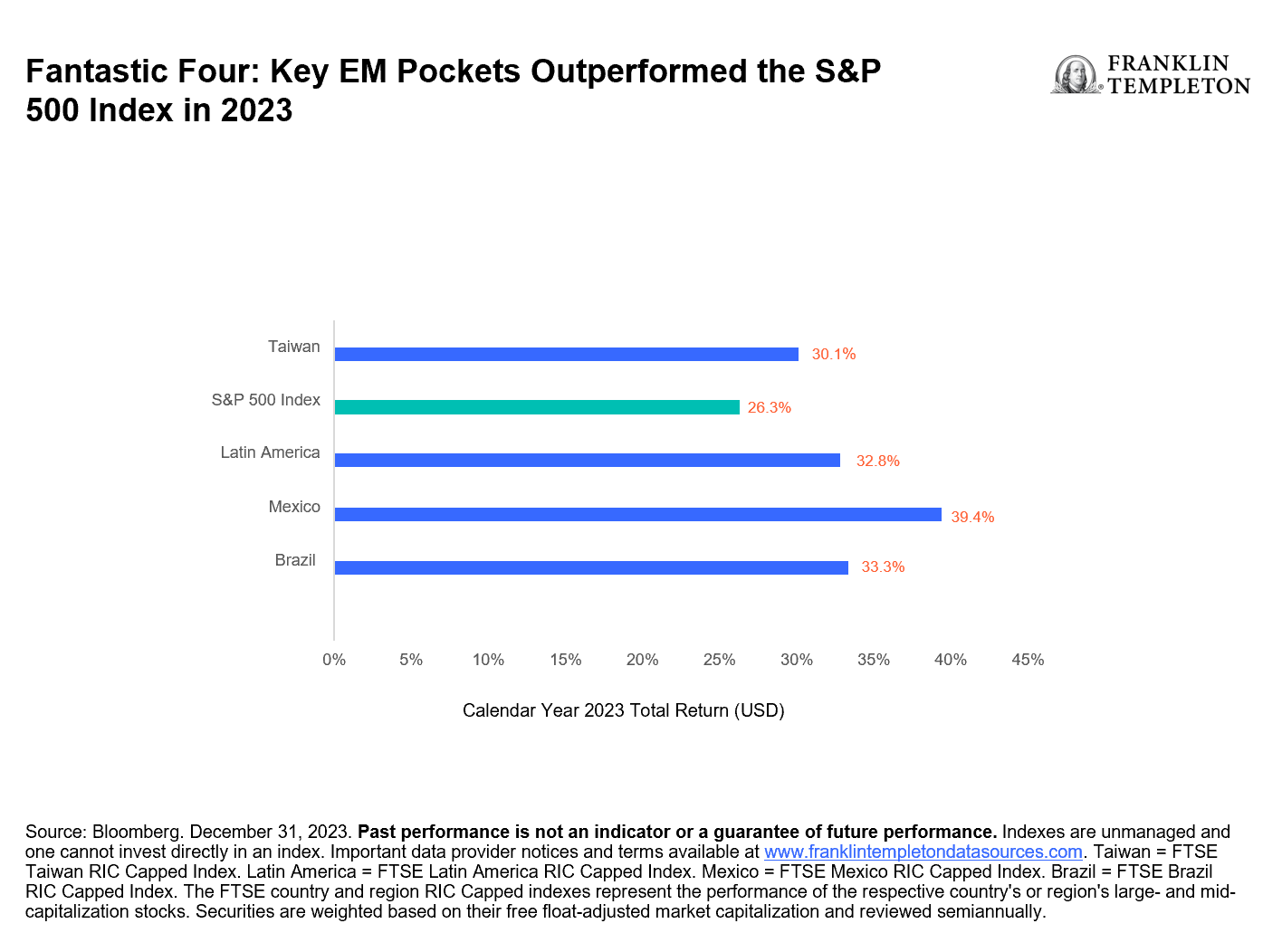

2023 outperformers

Instead of “Mag7,” perhaps “Fantastic Four” can catch on as a moniker for four pockets within EM markets that outperformed the S&P 500 Index last year. They are Taiwan, Mexico, Brazil and Latin America, which predominantly consists of its two largest economies.

Excluding China, EM stocks (as measured by the MSCI Emerging Markets ex China Index) returned 20.1% in 2023,8 with Latin America (as measured by the FTSE Latin America RIC Capped Index) faring well, up 33% for the year.9 The equity markets of Mexico (39.4%, as measured by the FTSE Mexico RIC Capped Index) and Brazil (33.3%, as measured by the FTSE Brazil RIC Capped Index) were standouts, and in Asia, tech powerhouse Taiwan (30.1%, as measured by the FTSE Taiwan RIC Capped Index) also posted stellar performance.10 For investors wanting to capture both of Latin America’s largest economies, the FTSE Latin America RIC Capped Index has a combined weighting of more than 90% in Brazil and Mexico, and notably lacks exposure to Argentina. In recent years, China has cultivated a growing influence in Latin America with trade pacts, overseas foreign direct investment and loans playing a major role in its strengthened ties with the region. While India’s market slightly trailed the S&P 500 last year, it still exhibited robust growth and is increasingly seen as an appealing alternative to China among both businesses and investors.

When chips are down…

Looking ahead, analysts expect an ongoing resurgence in global semiconductor sales to continue boosting Taiwan’s market. Powered by artificial intelligence and 3D tech, the chips revenue comeback is forecast to see a low to mid-teens percentage increase this year.11 Furthermore, to meet growing demand in key markets, Taiwan’s most valuable chip giant plans to expand its global footprint. In collaboration with Sony and Toyota, Taiwan Semiconductor Manufacturing has new plans to build a second plant in Japan.

In January, Taiwan saw its overall exports expand for a third consecutive month with an 18% year-over-year rise.12 During the month, the ruling Democratic Progressive Party’s (DPP) retention of the presidency in Taiwan’s recent elections appeared to support continuity in its economic policy. Although cross-straits relations continue to pose risks, markets had largely factored in the pro-independent DPP’s narrow victory.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal. International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Investments in companies in a specific country or region may experience greater volatility than those that are more broadly diversified geographically.

The government’s participation in the economy is still high and, therefore, investments in China will be subject to larger regulatory risk levels compared to many other countries. There are special risks associated with investments in China, Hong Kong and Taiwan, including less liquidity, expropriation, confiscatory taxation, international trade tensions, nationalization, and exchange control regulations and rapid inflation, all of which can negatively impact the fund. Investments in Taiwan could be adversely affected by its political and economic relationship with China.

ETFs trade like stocks, fluctuate in market value and may trade above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns. ETF shares may be bought or sold throughout the day at their market price on the exchange on which they are listed. However, there can be no guarantee that an active trading market for ETF shares will be developed or maintained or that their listing will continue or remain unchanged. While the shares of ETFs are tradable on secondary markets, they may not readily trade in all market conditions and may trade at significant discounts in periods of market stress.

Commissions, management fees, brokerage fees and expenses may be associated with investments in ETFs. Please read the prospectus and ETF facts before investing. ETFs are not guaranteed, their values change frequently, and past performance may not be repeated.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

__________

1. Source: “China Overtakes Japan As World’s Biggest Vehicle Exporter.” Barron’s. January 31, 2024.

2. Sources: Xinhua news agency, China Passenger Car Association.

3. Source: “How China became a car-exporting juggernaut.” The Economist. August 10, 2023,

4. Source: BloombergNEF.

5. The Magnificent Seven are (Mag7) Apple, Amazon, Alphabet, Meta, Microsoft, Nvidia and Tesla.

6. Source: FTSE Russell, February 13, 2024. The FTSE Emerging Index provides investors with a comprehensive means of measuring the performance of the most liquid large- and mid-cap companies in the emerging markets. Indexes are unmanaged and one cannot invest directly in an index. Important data provider notices and terms available at www.franklintempletondatasources.com.

7. Source: MSCI, January 31, 2024. The MSCI AC Asia ex Japan Index captures large- and mid-cap representation across two of three developed market countries (excluding Japan) and eight emerging market countries in Asia. Indexes are unmanaged and one cannot invest directly in an index. Important data provider notices and terms available at www.franklintempletondatasources.com.

8. Source: Bloomberg, as of December 31, 2023. The MSCI Emerging Markets ex China Index captures large- and mid-cap representation across 23 of the 24 emerging market countries excluding China. Past performance is not an indicator or a guarantee of future performance. Indexes are unmanaged and one cannot invest directly in an index. Important data provider notices and terms available at www.franklintempletondatasources.com.

9. Source: Bloomberg, as of December 31, 2023. The FTSE country and region RIC Capped indexes represent the performance of the respective country’s or region’s large- and mid-capitalization stocks. Securities are weighted based on their free float-adjusted market capitalization and reviewed semiannually. Past performance is not an indicator or a guarantee of future performance. Indexes are unmanaged and one cannot invest directly in an index. Important data provider notices and terms available at www.franklintempletondatasources.com.

10. Ibid.

11. Sources: Deloitte, Semiconductor Industry Association, Gartner, Inc.

12. Source: Ministry of Finance, Republic of China, February 2024.