Three Things We’re Thinking About Today

- Chinese internet stocks have struggled in recent weeks amid tighter regulatory scrutiny, higher US Treasury yields and block trades linked to a troubled hedge fund. China’s increased emphasis on fair competition, consumer protection and data security within the internet industry has been a chief concern. Though regulatory news could drive near-term share-price volatility, we remain largely confident in the longer-term fundamentals of several leading internet companies. These companies have grown rapidly by offering superior user experiences and efficiencies, and we expect these strengths to continue underpinning their structural earnings power. We also think that regulators are keen to ensure the sustainable development of the internet space for all stakeholders, rather than curb its growth. We are mindful of the dispersion in valuations across the internet space, and we seek to invest in quality companies trading below what we consider to be their intrinsic worth.

- Brazil’s fiscal challenges have returned to the spotlight as an intensifying pandemic adds pressure on the government to ramp up already-massive spending. Concerns about the country’s mounting debt burden have weighed on its stock market and currency. Complicating matters, rising domestic inflation has narrowed the scope for monetary policy support. The central bank raised its key interest rate from a record low in March, signaling the start of a rate-hike cycle. We believe that Brazil’s economic recovery will rely heavily on the government’s ability to implement long-awaited structural reforms. Meanwhile, as a major commodity exporter, Brazil is likely to benefit from rising prices for commodities, as well as their broad appeal as an inflation hedge. We expect higher interest rates in Brazil to bode well for banks, especially market leaders that have weathered the pandemic with the help of strong capital positions and large deposit franchises.

- The global competitiveness of emerging market (EM) companies has been a standout feature amid market swings and pandemic worries. A widespread chip shortage has underscored the world’s reliance on Taiwanese and South Korean semiconductor firms, which have dominated the global industry with their strong manufacturing capabilities. South Korean battery makers have become key suppliers of electric vehicle (EV) batteries, supporting EVs’ growing penetration on the back of favorable policies and advancing technology. Chinese biotechnology companies working on innovative treatments for cancer and other major diseases have reaped growing success in licensing their new drugs to global pharmaceutical firms. Across industries, we have found increasing evidence of EM companies scaling the value chain, and we see durable growth characteristics in many of them.

Outlook

Fresh waves of COVID-19 infection have continued to test economies and health care systems globally, just as more countries step up the rollout of vaccines. We think EMs will likely stay resilient in the face of new challenges. Many EMs have remained less leveraged than developed economies at the sovereign, corporate and household levels. EM banking systems have largely withstood stress despite loan moratoriums. Technology and consumption have also become new drivers of economic growth for many EMs.

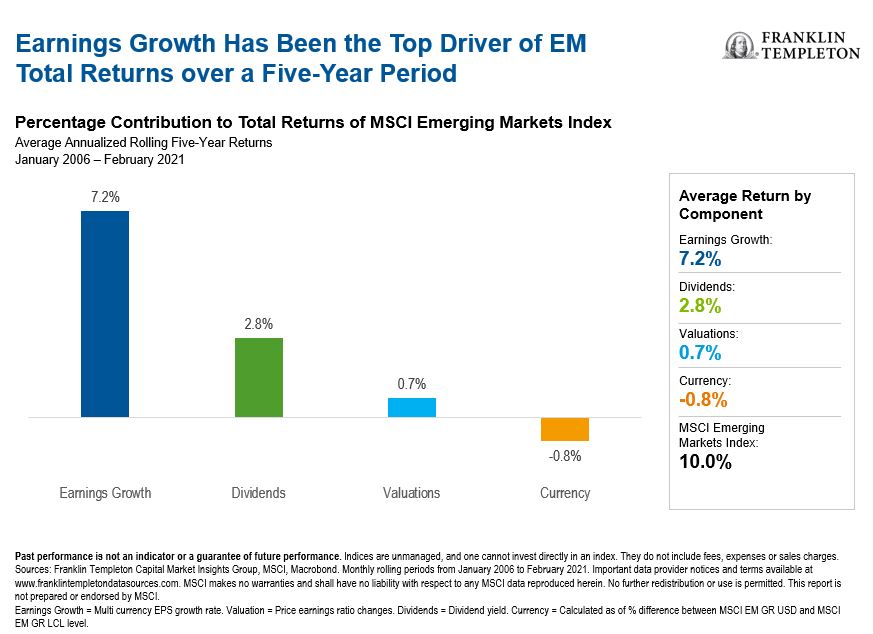

We expect a sharp earnings rebound in EMs this year from a low base last year. According to our analysis, EM earnings have been the top driver of total returns in the MSCI Emerging Markets Index historically (see accompanying chart). Notably, digital transformation and innovation—which accelerated during COVID-19—have translated into higher free cash flow generation. This cash flow has helped deleverage balance sheets. It has also found its way back to investors through dividends and share buybacks, and encouraged companies to adopt improved governance standards and better capital discipline. In our view, these all add up to a higher quality earnings story in EMs.

Reflationary expectations and higher US bond yields have stoked market volatility. Though inflation has picked up from low levels last year amid recovering economic activity, firmer commodity prices and near-term supply chain bottlenecks, we believe considerable slack remains in many economies, especially on the labor front. Also visible to us are longer-term deflationary risks arising from technology advancements and demographic headwinds. Rather than position for specific macroeconomic scenarios, we strive to build well-diversified portfolios that can potentially navigate a range of market environments.

A long-term, stock-driven, and valuation-aware focus is central to our investment approach. We seek companies with sustainable earnings power, trading at discounts to our perception of their intrinsic worth. We have found many such companies operating in areas of secular growth related to technology and consumption. Of particular appeal to us are business models and management teams that display agility and resilience in a fast-changing world.

Emerging Markets Key Trends and Developments

EM equities rose over the first quarter but lagged developed market stocks. Gains in the early part of the quarter cushioned EMs from losses in the final weeks, as optimism around increased US stimulus, COVID-19 vaccination drives and improved economic prospects waned amid concerns over rising inflation, higher US Treasury yields and resurgent outbreaks. EM currencies broadly weakened against the US dollar. The MSCI Emerging Markets Index rose 2.3% over the quarter, while the MSCI World Index returned 5.0%, both in US dollars.1

The Most Important Moves in Emerging Markets in the First Quarter of 2021

Emerging Asian equities finished the quarter higher despite weakness in March. Taiwan’s technology-heavy index rallied over the three-month period as the economy benefited from strong technology exports. Indian equities climbed. An expansionary fiscal budget, an inoculation campaign and stronger economic activity helped investors look past rising COVID-19 cases in the country. Conversely, China’s market fell after shedding early gains. Caution around monetary policy, stock valuations, US-China tensions and increased regulatory scrutiny of Chinese internet firms overshadowed a continued economic recovery. Stocks in the Philippines slid as a widening contagion led to renewed restrictions in the country’s capital.

Latin American equities fell over a volatile quarter. Brazilian stocks retreated amid a jump in COVID-19 cases, growing fiscal concerns, signs of increased state interference in the economy and heightened political noise ahead of next year’s presidential election. The Brazilian real weakened. In Peru, equities declined as a new wave of outbreaks added to uncertainty around the country’s presidential election in April—polls suggested no clear favorite to win the race. In contrast, Mexican equities gained. Mexico’s central bank raised its economic growth forecast for the year, thanks in part to a stronger outlook for US industrial activity.

Markets across Europe, the Middle East and Africa recorded a strong quarter as a whole. An upswing in oil prices buoyed Russian equities, although worries of potential US sanctions against Russia checked returns. Higher oil prices also provided a positive backdrop for Saudi Arabia’s market. South African stocks rallied on firmer commodity prices, the country’s vaccination drive, and a reopening economy. However, Turkish equities tumbled, as did the lira. Turkey’s president dismissed the central bank’s governor shortly after it announced a sharp interest-rate hike to tame inflation, igniting fears of a premature return to looser monetary policy in the country.

Regional Outlook

Scroll over the map to view comments on the countries indicated and our sentiment.

Green = positive, Red = negative, Blue = neutral

The graphic reflects the views of Franklin Templeton Emerging Markets Equity regarding each region and are updated on a quarterly basis. All viewpoints reflect solely the views and opinions of Franklin Templeton Emerging Markets Equity. Not representative of an actual account or portfolio.

| ISO Code | Country | Sentiment Score | Opinion |

|---|---|---|---|

| CN | China | 0.5 | The government’s policy response is likely to soften the impact of COVID-19. China seems to be on its way to being the first to recover, barring new waves of infection. We believe China will likely emerge stronger from this crisis. |

| IN | India | 0.5 | Long-term fundamentals remain robust in view of increasing consumer penetration, growing formalization of the economy, a reform push and a stable government. However, near-peak market valuations have offset a strong earnings revival outlook. |

| ID | Indonesia | 1 | The 12-month outlook appears more constructive than a quarter ago. Progress in the country’s vaccination program should aid the economy’s reopening. Government reforms could support private investments, while stimulus measures such as cash handouts could bolster consumption. |

| KR | South Korea | 0.5 | Macro indicators have deteriorated after the onset of COVID-19 but should normalize post the pandemic. Concerns about government regulations have grown. Escalating geopolitical tensions with North Korea warrant close attention. |

| TW | Taiwan | 1 | Signs of demand recovery for some technology-related products should be positive for Taiwan’s export- and technology-oriented economy. US-China relations might be past their nadir, which should help business confidence. Although stretched market valuations could lead to short-term market declines, the longer-term outlook remains positive, given fifth generation wireless technology (5G) deployment and an acceleration of production relocations from China. |

| TH | Thailand | 1 | The overall outlook appears constructive, thanks to good pandemic management and progress in vaccine rollouts. A reopening domestic economy should drive consumption, though a weak tourist arrival outlook and political concerns could be partial drags. A global economic recovery should support exports. |

| PL | Poland | 0.5 | Broad economic sentiment strengthened month-on-month in February, though it remained below its pre-pandemic level. Sentiment improved even in areas that COVID-19 hit most—retail and services—as consumer confidence grew. Inflation expectations have reaccelerated this year, with labor market indicators reflecting tighter conditions. |

| CZ | Czech Republic | 0.5 | Broad economic sentiment, while still weak, showed a month-on-month upturn in February. Improvements were in manufacturing and construction, while COVID-19 continued to impact consumption. We expect economic growth this year, while inflation could see a temporary spike due to a low-base effect. |

| HU | Hungary | 0.5 | General sentiment has continued to signal the economy’s recovery. Hungary’s labor market has shown one of the broadest improvements compared with its closest Central European peers. Inflation accelerated in February, and we see the potential for it to breach the upper bound of the central bank’s target range in the near term. |

| RU | Russia | 1.0 | In a stable commodities/ruble environment, companies should benefit from positive earnings revisions and improved distributions to shareholders. Potential sanctions from the United States or European Union remain a key risk. |

| BR | Brazil | 1 | The pandemic could have a lasting impact on Brazil’s economy. The speed and strength of its recovery is likely to depend on the government resuming its ambitious economic reforms, which should underpin higher long-term economic growth and a better business environment. Low interest rates should continue driving domestic investor flows into equities. However, political uncertainty and mixed economic signals could sustain market volatility. |

| MX | Mexico | 1 | Mexico has an open economy that is heavily exposed to the United States (most of Mexico’s exports head there). A solid US recovery has driven a rebound in Mexico’s economic activity. However, the duration of COVID-19 restrictions in Mexico could still determine the strength of the recovery. |

| PE | Peru | 0.5 | Political volatility has been hindering Peru’s economic recovery, shifting focus away from government spending and infrastructure investment. Continued political noise in the lead-up to this year’s general election seems likely. Nonetheless, investor flows into EMs and commodities could be a tailwind. |

| KW | Kuwait | 0 | Kuwait has a strong fiscal position. However, a delay in reforms, including the issuance of a debt law, could erode government finances and potentially impact the economy through a slowdown in capital expenditure. The non-oil economy has remained somewhat shielded as most Kuwaitis are employed by the government. We are mindful of relatively rich market valuations and a weak growth outlook. |

| SA | Saudi Arabia | 0.5 | The outlook appears to be improving but remains anchored to a normalization of economic activity, a recovery in oil prices and government/public investment fund (PIF) spending. Substantial foreign exchange reserves and PIF assets provide some comfort. |

| AE | United Arab Emirates | 0.5 | The market is cheaper than its Middle Eastern and North African peers amid its higher dividend yield. Cyclical stocks (especially in Dubai) could re-rate as a vaccination program leads to better mobility. |

| EG | Egypt | 1 | The economy has continued to grow. Discretionary spending has been under some pressure but appears to be recovering gradually. Receding inflation could pave the way for further interest-rate cuts. We expect the currency to remain largely stable. An extended disruption in tourism—a source of foreign currencies—could be a key risk, though the government has so far provided support. |

| KE | Kenya | 1 | The outlook is starting to improve, with what appears to be a faster recovery in economic activity. |

| NG | Nigeria | 0 | The risk of further currency weakness remains high, and weak political and macroeconomic conditions are likely to create a weak environment for stocks. |

| ZA | South Africa | 0.5 | The broad outlook appears to be improving given the economic recovery and some positive news on reforms. However, we think a long-term recovery is still dependent on the government’s ability to implement and commit to other reforms. |

| QA | Qatar | 1 | Activities related to FIFA 2022 preparations and liquefied natural gas production expansion present a case for growth and earnings upticks for the next three to four years. High sovereign reserves and a low oil budget breakeven point are also positives. We think Qatar offers stability, though full market valuations could limit investment opportunities. |

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments. Smaller and newer companies can be particularly sensitive to changing economic conditions. Their growth prospects are less certain than those of larger, more established companies, and they can be volatile.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. All investments involve risks, including possible loss of principal.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

_______________________________

1. Source: MSCI. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-market countries. The MSCI World Index captures large- and mid-cap performance across 23 developed markets. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.