The reflation theme has become investors’ main focus of attention lately. This is particularly true in developed markets (DMs), which face a rapid acceleration of domestic demand amid surging commodity prices—including energy.

But the situation across emerging markets (EMs) is more varied. Many of these countries lack the fiscal space and central-bank firepower of their DM counterparts. They are therefore seeing a weaker improvement of their labor markets and a slower narrowing of their output gaps.

On the one hand, the speed of emerging markets’ recoveries will greatly depend on the progress of their respective vaccination programs, as many EMs continue to face vaccine supply shortages. On the other hand, some of them are highly vulnerable to commodity price shocks, particularly foodstuffs, as these items represent a large fraction of their Consumer Price Index (CPI) baskets, while others are more vulnerable to exchange rate (FX) volatility.

EM Inflation: A Transitory Phenomenon?

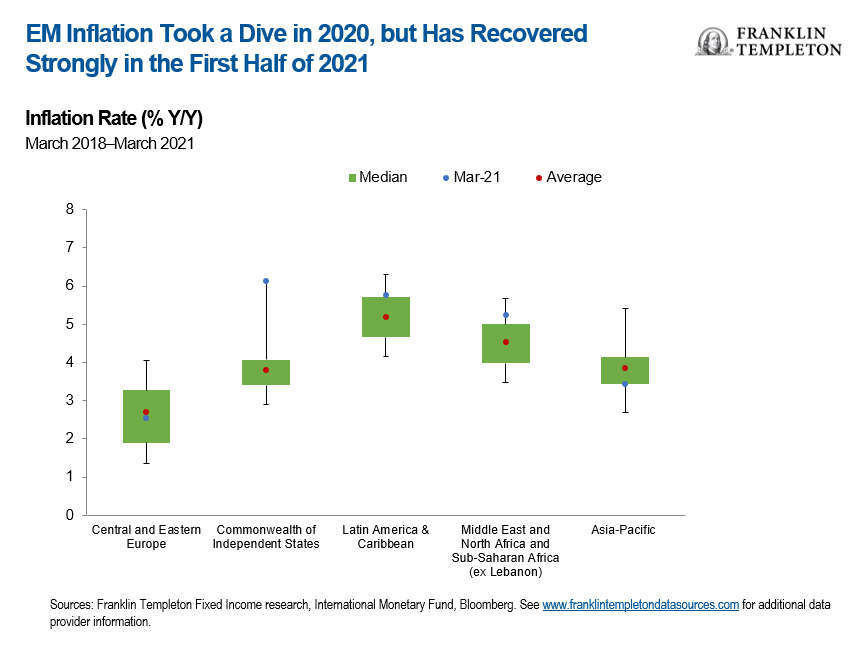

The inflation story in emerging markets remains highly differentiated, but the pandemic caused a sharp decline that was felt across all regions. While in 2019 aggregate EM inflation averaged 4.6% year-on-year (Y/Y), it fell to just 3% Y/Y in May 2020. A large part of the decline was driven by mainland China, where headline inflation fell from 5.4% Y/Y in January 2020 (the highest level since 2011, led by a surge in food prices) to 4.3% in May, declining to a trough of -0.5% in November. By May 2020, inflation had dropped ca. 1.6 percentage points (pp) in the Asia-Pacific (APAC) region (to 3% Y/Y). The Central and Eastern Europe (CEE) and Latin America (LatAm) regions also saw sizeable inflation declines from end-2019, albeit less pronounced than APAC. By contrast, the CPI drop in the Middle East and North Africa (MENA) & Sub-Saharan Africa (SSA) region (excluding Lebanon) proved more gradual, while in the Commonwealth of Independent States (CIS) it remained fairly contained.1

Since its trough in the second quarter (2Q) of 2020, inflation across emerging markets has accelerated at different paces. The steepest acceleration has been observed in the CIS region, where March 2021 inflation marked a three-year high of 6.1% Y/Y. Two countries largely drove this strong increase: (1) Ukraine (+6.8 pp increase since 2Q’20 to 8.5% Y/Y) due to a surge in food prices from a bad harvest, rising energy prices and a jump in the minimum wage; and (2) Belarus (+3.6 pp increase since 2Q’20 to 8.5% Y/Y) due to strong FX pass-through effects, food price increases, and more recently an increase in some regulated prices and tariffs. The dynamics in MENA and LatAm were less pronounced, but inflation is now above its respective three-year average and median levels. Meanwhile, inflation in CEE and APAC has accelerated slowly and remains below its 2019 levels. Weak Chinese inflation (0.9% Y/Y in April) continues to drag APAC inflation lower, but we expect it to gradually accelerate as global demand for Asian goods recovers.

Low base effects from 2020 will accelerate EM inflation in 2Q’21-3Q’21, but other factors are impacting it simultaneously. Between now and year-end 2021, the International Monetary Fund (IMF) expects headline inflation to increase in MENA & SSA and APAC, but decrease in the CIS and LatAm regions, particularly in those countries that have seen surges in food prices and currency weakness. Large output gaps will also exert downward pressures on inflation, especially in LatAm. By end-2021, inflation should be close to its 10-year average in all regions, except in the CIS where it will remain lower. Provided there are no significant deviations in the IMF inflation forecasts, these dynamics suggest that, on aggregate, inflation pressures are not as concerning as in DMs. However, the degree of inflation heterogeneity across EM countries is vast, and any regional generalization would paint an incomplete picture of inflation dynamics across EMs.

EM Inflation Drivers: Food, Energy, and FX Pass-Through

Food inflation has been rising across major emerging markets. However, several local factors impact food inflation, and the causes of higher prices have not been homogenous across regions. Inflation in items like fruit and vegetables in particular seems to vary across markets, due to local factors and climatic conditions for such items. More broadly, the IMF estimated in its latest report (April 2021) that the annual pass-through from international food prices to the domestic food CPI was much higher for middle- and low-income countries than for high-income countries (0.26 versus 0.14).2 This means that the impact on headline inflation is higher in EMs since food has a larger share in these countries’ CPI baskets. By comparison, food items in the United States and euro area represent 14% and 17.2% of their respective CPI baskets.3

Recently, agricultural prices have reached 10-year highs, but low base effects from 2020 point to a faster Y/Y acceleration over the next two quarters. This is particularly true for countries such as Brazil and Russia, where food inflation remains significantly above headline inflation. Within Central and Eastern Europe and Middle East and Africa (CEEMEA) markets, there are wider divergences. In Turkey, food inflation was as high as 17.8% Y/Y in March, led by oils and fats, fish and seafood. South Africa also saw elevated food inflation at 5.4% Y/Y, but low inflation for vegetables and fruit. Within Asia, food inflation was high only in a few markets, like the Philippines and India.4

The rise in energy prices and low base effects from 2020 will add further inflation pressures, but the (still large) negative output gaps will keep core inflation contained. Energy prices have fully recovered from their trough in 2Q’20 and are already feeding through the CPI baskets of many emerging markets. However, the pandemic caused one of the steepest contractions in gross domestic product (GDP) ever recorded and created deep output gaps. Domestic demand is expected to accelerate gradually as economies reopen and vaccination programs progress, but many countries have suffered deep structural damages to their already weak labor markets. The change in unemployment from 2019 levels is sizeable for many EMs but structurally, the damage is more severe given the level of shadow employment and the size of the informal economy in EMs.

We expect output gaps to narrow only gradually. Paired with our relatively stable FX expectations, this should help keep inflation expectations under control. But FX pass-through effects in many countries have proven sizeable, especially among large importers. Any additional bouts of EM currency selloffs will exert upward inflation pressures to this subset of countries, adding stress to inflation expectations over the short and medium run. Monitoring the financial account dynamics of these countries will therefore prove essential.

We conclude that inflation pressures, in general, are not a major concern for EMs, but need to be analyzed on a case-by-case basis and with special emphasis on countries’ respective output gaps.

We are not overly concerned by commodity-driven inflation, given that higher commodity prices tend to be correlated with stronger EM fundamentals. In addition, EM central banks can act quickly to counter more structural and persistent increases in inflation, given their low base rates and with liquidity measures at their disposal.

From an investment standpoint, current prices for EM inflation-linked bonds seem fair, in our opinion. Prices appear to warrant limited concern about a long-term impact from the recent uptick in inflation, which we expect to be temporary.

Want to learn more? Read the team’s more in-depth topic paper on this subject, with case studies in two emerging market countries.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Special risks are associated with investing in foreign securities, including risks associated with political and economic developments, trading practices, availability of information, limited markets and currency exchange rate fluctuations and policies; investments in emerging markets involve heightened risks related to the same factors. Sovereign debt securities are subject to various risks in addition to those relating to debt securities and foreign securities generally, including, but not limited to, the risk that a governmental entity may be unwilling or unable to pay interest and repay principal on its sovereign debt. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments. China may be subject to considerable degrees of economic, political and social instability. Investments in securities of Chinese issuers involve risks that are specific to China, including certain legal, regulatory, political and economic risks.

There is no assurance any estimate, forecast or projection will be realized.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained herein has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

_______________________________

1. Sources: National Central Banks, International Monetary Fund, Franklin Templeton Fixed Income Research.

2. IMF World Economic Outlook: Managing Divergent Recoveries, April 2021. There is no assurance that any estimate, forecast or projection will be realized.

3. Sources: Eurostat, US Bureau of Labor Statistics (as of May 2021).

4. Sources: National Central Banks. As of May 2021.