English

English Deutsch

DeutschThis post is also available in: German

China has seen rapid urbanization; as of 2020, 61% of its population lived in urban areas.1 In 1960, that number was a mere 16%.2 Evergrande benefited from—and helped fuel—this change by borrowing funds to sell property to the Chinese public long before these projects were complete. The firm eventually expanded into owning theme parks, bottled water and a soccer team. However, the Chinese government, under its “common prosperity” campaign, has sought to deleverage the sector in order to avoid a potential bubble, enforcing its “three red lines” policy on property developers while steering investor capital toward the manufacturing sector. As a result, Evergrande has not been able to recently service its debts, missing bond payments in late September, sparking fears of contagion among investors.

First, is Evergrande truly contained, or could this be a Lehman moment?

We believe the Evergrande situation will be contained. Insiders have commented that the Chinese government will step in if necessary to provide the needed guarantees, but only after making various stakeholders sweat it out and letting equity holders bear the brunt of the pain for excessive risk-taking. We’ve already observed some initial steps from the government that support our view in the form of buying Evergrande’s stake in a bank. Time and time again, the Chinese government has successfully navigated similar situations given its powerful centralized structure. Of course, if there is fraud or accounting irregularities with Evergrande, which is a distinct possibility, this might change the facts—and our outlook—but we think even then, the government would have the tools to handle the situation.

It is a re-election next year for President Xi, which provides extra motivation to exert as much power as needed to make sure any Evergrande asset sales go smoothly.

There is a laundry list of reasons why (and how) the Chinese government may respond differently to a financial crisis than the United States. Unlike the United States, the Chinese government controls its banks, which are encouraged to prioritize the Chinese economy over their own profitability, and the government has access to their deposits. The Chinese government also controls the movement of funds across its borders, as well as the courts. Given the reach of the government, it can instruct state-owned real estate and construction companies to help complete Evergrande’s 800 unfinished property complexes. China’s “common prosperity” campaign has been recently touted by President Xi Jinping, and it would seemingly be a priority to protect homebuyers and certain investors from losses and preserve the integrity of the property sector considering its systemic importance to the economy. Lastly, the government can manage public perception and response, both in its control of the media and by curbing public demonstrations.3

Additionally, our view is that there are plenty of assets to cover Evergrande’s debt if asset sales are managed in a controlled fashion, based on conversations with various professionals with deep knowledge of China within Franklin Templeton and external restructuring experts. More importantly, it is a re-election next year for President Xi, which provides extra motivation to exert as much power as needed to make sure any Evergrande asset sales go smoothly.

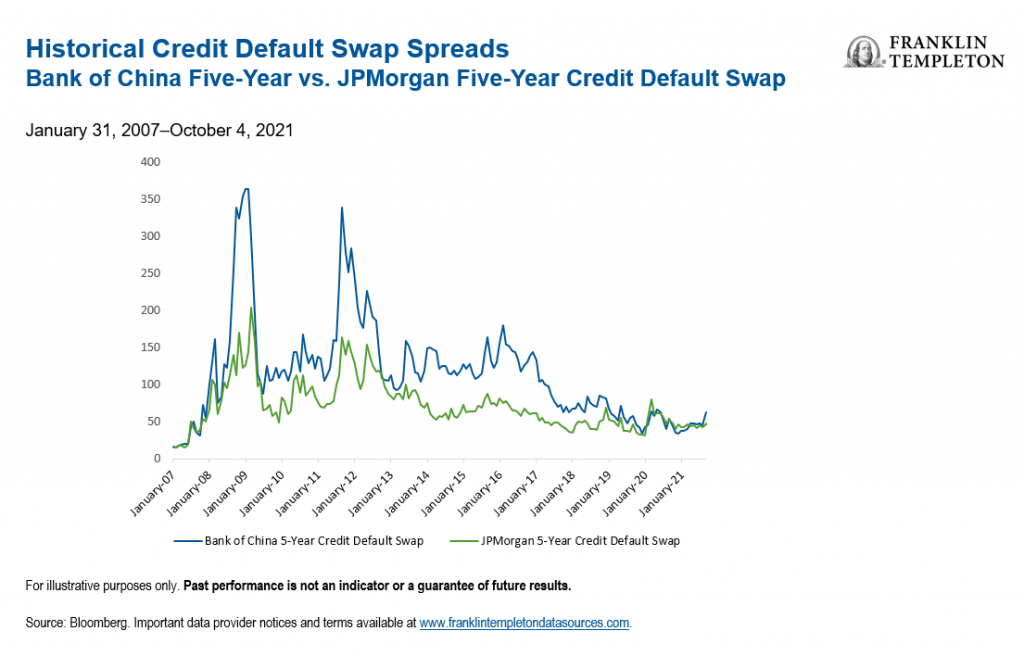

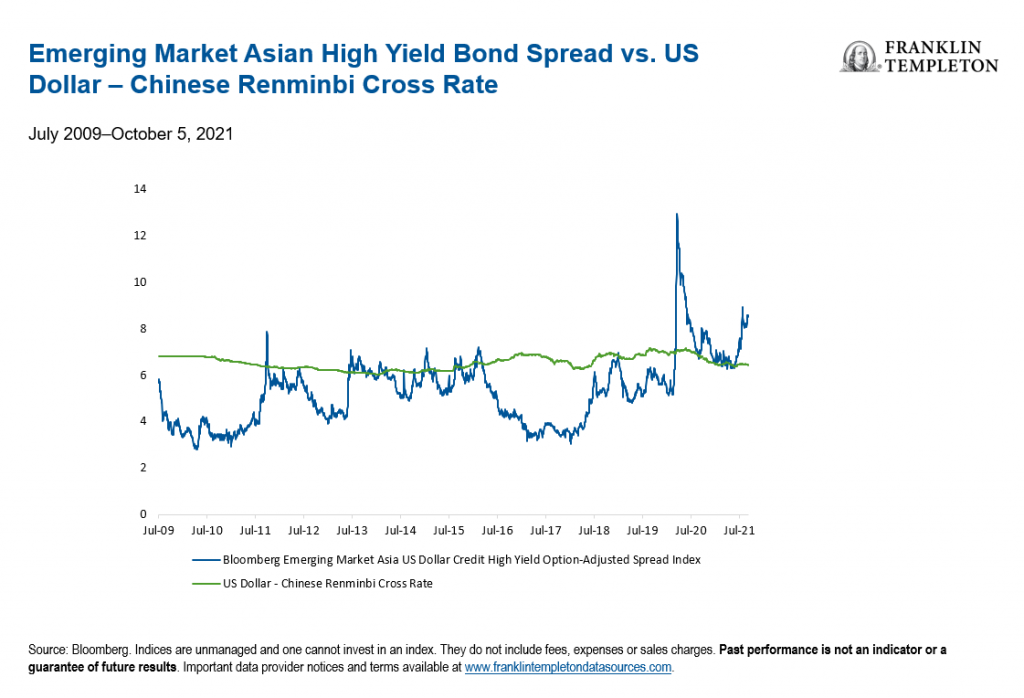

Lastly, when looking back to the global financial crisis, we saw credit default swap spreads widen drastically and currency volatility spike, indicating that banks and investors were put on their heels in response to a potentially dramatic crisis. Here, we have not seen credit default swap spreads move too much for US or Chinese banks (see first chart below), nor has there been a lot of currency volatility in the renminbi (see second chart below), most likely indicating a very different set of circumstances and a commensurately different outcome.

Should this become more systemic, the government would also have traditional levers to inject liquidity, such as the additional reserve requirement ratio (RRR) cut that was initiated in July.

Second, what would a slowdown in the Chinese property market mean for global growth?

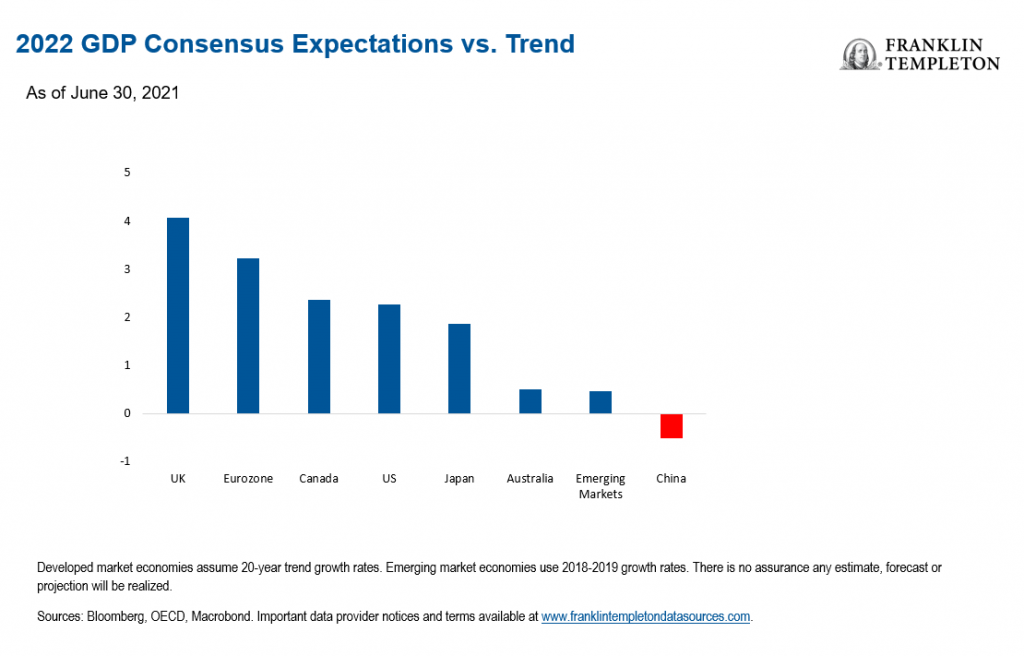

In part due to the reasons stated above, the ramifications related to Evergrande will likely have limited global impact. We believe China is likely to experience below-trend growth in 2022 when compared to other regions (see chart below).

As we think about the outlook for China and its impact on the global economy, the recent meaningful regulatory shift we’ve seen this year across a number of industries (for “common- prosperity”) deserves keen focus. There are specifics risks to watch out for as the government exerts more regulatory influence. One strong example is the recent elevation of de-carbonization initiatives, and the resulting intervention in industries that conflict with that stated goal by consuming too much power.

Regarding the property sector, could the government’s orchestrated slowdown get amplified in a way that escapes its control? Certainly, that is not out of the realm of possibility, in which case China would underperform growth expectations and may warrant further scrutiny. Then again, it’s possible that the markets more recently have been underestimating China’s ability to once again intervene and engineer a favorable outcome. Taking a broader perspective, foreign capital and investor confidence is also a wildcard. Will foreign investors withdraw as we continue to see more regulatory and sectoral shifts by the government? So far, the answer has been “no,” but we are in the early stages of a continued transformation of China which will extend for many years to come.

We have thought for a while that the dramatic widening in Asian high yield corporate spreads this year foreshadowed a number of forthcoming defaults. However, there are likely to still be a few surprises that catch investors off guard—such as the recent Fantasia default—that suggests some property developers may become increasingly grim about future growth prospects and throw in the towel. This sentiment amongst developers bears watching in terms of how widespread and infectious it becomes. We also need to ensure there aren’t widespread hidden liabilities among other property developers. Should these additional risks materialize across the entire sector, it would clearly destroy confidence and become a formidable challenge for the government to overcome.

Ultimately, we believe China will provide a form of bailout to Evergrande (creating moral hazard), in order to preserve broader financial stability and “common prosperity,” continuing to walk the tightrope between that prosperity and pressuring developers to de-leverage and avoid excessive risks. While Evergrande itself may not be too big to fail, despite its gargantuan size, we believe the Chinese property sector is certainly too big to fail given that it represents almost 30% of China’s GDP, and by some estimates 60% – 70% of the average household’s net worth. We are keenly monitoring this situation for its global, and multi-asset, implications.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with investing in foreign securities, including risks associated with political and economic developments, trading practices, availability of information, limited markets and currency exchange rate fluctuations and policies; investments in emerging markets involve heightened risks related to the same factors. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments. China may be subject to considerable degrees of economic, political and social instability. Investments in securities of Chinese issuers involve risks that are specific to China, including certain legal, regulatory, political and economic risks.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

There is no assurance any estimate, forecast or projection will be realized.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

______________________________

1. Source: United Nations Population Division. World Urbanization Prospects: 2018 Revision.

2. Ibid.

3. Source: K. Bradsher. “How China Plans to Avert an Evergrande Financial Crisis,” The New York Times, September 26, 2021.