English

English Español

Español

This post is also available in: Spanish

Franklin Templeton Investment Solutions Asset Allocation Backdrop

As we look back on 2021, a year of strong global growth and outsized equity returns, it’s easy to point to China as a notable laggard. At 3.6% of the global equity market (using the MSCI ACWI Index) and 32.4% of the emerging markets equity universe (using the MSCI Emerging Markets Index)1, Chinese firms have seen their share of the global market capitalization slip while overseas markets have rallied.

Over the course of the past calendar year, the Chinese offshore equity market (proxied by the MSCI China Index, unhedged) returned -21.7% on the back of slowing domestic growth, restrictive zero-COVID-19 tolerance policies, and a wave of regulatory announcements that have weighed negatively upon Chinese equity markets. Furthermore, from the February 16, 2021, peak to current levels, the MSCI China index has sold off by roughly -35% (as of January 10, 2022). This comes on the back of a calendar 2020 that delivered much better returns for investors in Chinese equities, as China was one of the first nations to emerge from the depths of the initial COVID-19 crisis.

With the rest of the world playing catch-up for much of the past calendar year, global investors are confronted with an important question: Is now the right time for unconstrained global investors to embrace a more constructive view of Chinese equities? We believe the short answer to this question is no, but as with most things, it’s not a simple answer.

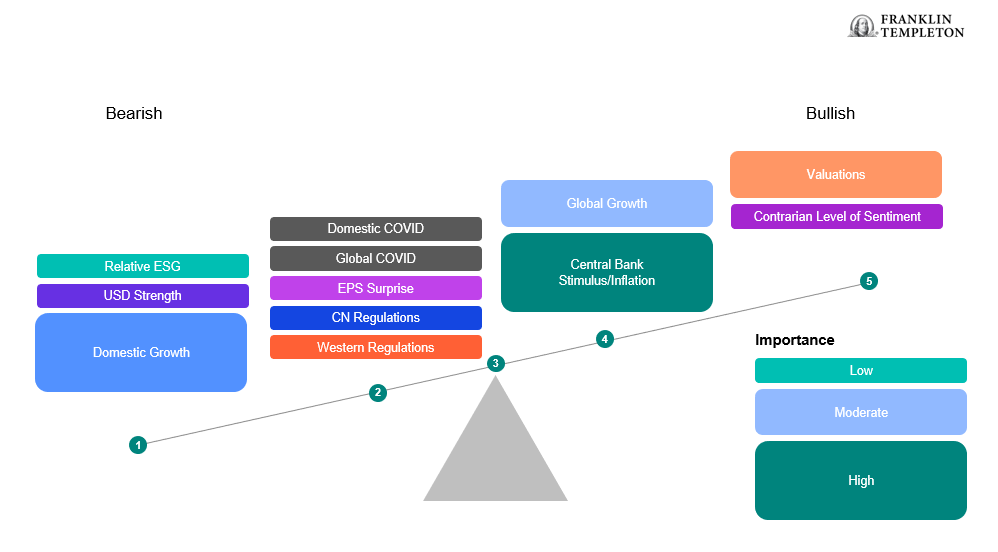

Below, you can find an infographic that frames the range of our current thinking toward the Chinese equity market.

Our Negative Outlook Holds for Now

Several key factors that have driven our more pessimistic stance remain firmly in place:

- Regulatory clampdowns show few signs of abating.

- Property sector weakness is likely to persist.

- Leverage looks elevated across much of the Chinese private sector, from banks to housing-related names to broader state-owned enterprises.

- Relationships with Western nations remain frayed, with many hurdles ahead.

- Dollar strength, on the back of accelerated Federal Reserve tapering/tightening, has the potential to weigh on returns.

- Elevated commodity prices, weak headline consumption figures, and energy shortages that have hampered factory production cause domestic gross domestic product growth to face a continued uphill battle.

This view all plays into the theme we’ve adopted for the region since the onset of COVID-19—namely, that China would be first-in, first-out in terms of their economy’s growth recovery. What we are observing today is the after-effects of this trend, as the rest of the world plays catch-up with China’s recovery last year.

While we have seen some positive news stories over the past months around the regulatory space, such as smaller-than-anticipated anticompetitive fines and Alibaba Group co-founder Jack Ma’s international travel forays, they continue to be met by offsetting clampdowns. Over the past two months, technology firms’ advertising revenues have come under pressure, new video game and mobile app releases remain largely frozen, Alibaba’s investments in third-party companies have received increased scrutiny, and Chinese ride-hailing company Didi has been forced to delist from the US stock market. As it currently stands, large Chinese technology firms are still in the eye of the storm.

Geopolitical tensions are another key headwind worth highlighting, particularly as it relates to the United States. While recent headlines have noted the prospects of the US Biden administration easing tariffs on China following his summit with Chinese President Xi Jinping, this masks issues that have yet to be worked out. As the US-China relationship remains heavily strained, this has the potential to suppress consumer confidence and business investment over the coming months across China.

Green Shoots: What Could Sway Our Position?

However, in light of the dramatic underperformance that we’ve observed out of China since the market peak last February, there are some green shoots vying for our attention. First and foremost, as we enter a meaningful election year leading up to the National Party Congress, we expect a continuation of easy policy. This applies not just to the People’s Bank of China, which has already embarked on an easing cycle, but also fiscal policy. As common prosperity remains a focal point of President Xi’s policy, we expect easy fiscal policy to accelerate over the coming months, likely providing a meaningful boost to weak consumption activity.

In spite of suppressed consumption activity, it appears that other parts of the Chinese economy show more resilience. The lockdowns that the Chinese government has rolled out in response to rising COVID-19 cases has yet to completely hamper industrial production and Chinese exports, which sit at healthy levels. The China Manufacturing Purchasing Managers’ Index has additionally bounced back to and risen above 50, a level typically consistent with accelerating manufacturing growth.

Equity multiples likewise appear unsustainable. At its peak on February 17, 2021, the trailing price-earnings (P/E) ratio of the MSCI China Index was 24.7x; that has plummeted to 14.4x (as of January 10, 2022).2 This drop has been led by the tech, communication services and media sectors. We have potentially seen the worst of the regulatory clampdowns for these industries, with many disciplinary fines smaller than feared. Although the focus on common prosperity is likely to impose structural downward pressure on valuations, it is highly unlikely that the “economic Golden Geese,” whether that be names like Alibaba, Tencent, or Meituan, will be stifled.

Multi-Asset Allocation Implications

Within Franklin Templeton Investment Solutions’ Asset Allocation research team, we currently find ourselves with an unfavorable outlook on both the Chinese equity market and economy relative to other regions around the globe. This has been the case since shortly after the Chinese equity markets peaked last February.

However, as we embark on a new year with a significant amount of bad news already priced into the equity market, the debate around China has gathered momentum. While we believe it is still too early to begin dipping our toes back into the Chinese markets, we could foresee a more favorable stance unfolding over the coming months on the back of easy policy and potentially excessive bearishness priced into the market.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with investing in foreign securities, including risks associated with political and economic developments, trading practices, availability of information, limited markets and currency exchange rate fluctuations and policies; investments in emerging markets involve heightened risks related to the same factors. Investments in fast-growing industries like the technology and health care sectors (which have historically been volatile) could result in increased price fluctuation, especially over the short term, due to the rapid pace of product change and development and changes in government regulation of companies emphasizing scientific or technological advancement or regulatory approval for new drugs and medical instruments. China may be subject to considerable degrees of economic, political and social instability. Investments in securities of Chinese issuers involve risks that are specific to China, including certain legal, regulatory, political and economic risks.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

________________________________________

1. Information is as of 12/31/21. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

2. Source: Bloomberg. Indexes are unmanaged and one cannot directly invest in them. Past performance is not an indicator or a guarantee of future results.