English

English Italiano

Italiano Español

Español

This post is also available in: Italian, Spanish

by Franklin Templeton Emerging Markets Equity team

Investors’ worst fears about Russia’s intentions toward Ukraine have materialized following Russian President Vladimir Putin‘s announcement that he is sending troops into the country to “demilitarize” the nation. This follows his recognition of the Lugansk People’s Republic and the Donetsk People’s Republic as independent and sovereign states. There was a period when the crisis could have been resolved by negotiations and diplomacy, and possible limited penetration by Russia into rebel held territories in Ukraine.

We are monitoring developments very closely, with the twin goals of being risk-aware and prioritizing client interests.

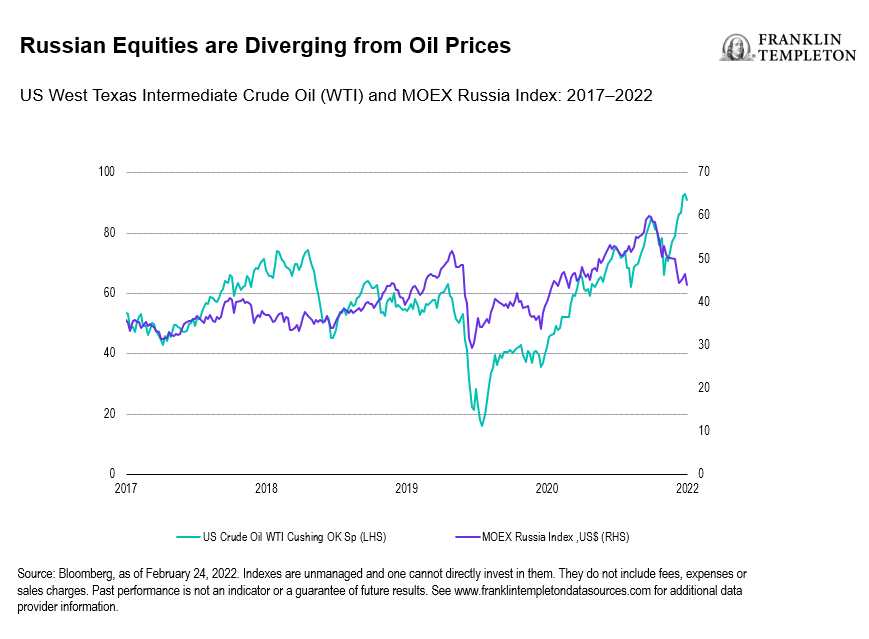

Following a 14% rally in the MSCI Russia Index in 2021, the index has posted double-digit declines in 2022 as investors factor in the risk of sanctions, dividend cuts and higher risk premiums.1

Our view on investments in Russian companies prior to this strife was constructive, with diversified exposure to the market, including in the energy and financial sector. The market is now more focused on the conflict than investment opportunities in the economy.

The invasion of Ukraine is testing our conviction, but our views are unchanged for now, acknowledging this will put short-term pressure on performance. Our previous focus was on Russian corporates with strong fundamentals: high return on equity, low valuations, and what we viewed as superior earnings growth prospects. Nevertheless, in the short term these fundamentals can be undermined by recent actions, which can drive up volatility and the cost of equity and exert downward pressure on returns.

Individual company sanctions by the United States and European Union represent a risk we see. These could limit liquidity and impact companies’ ability to pay dividends—and limit foreign investment.

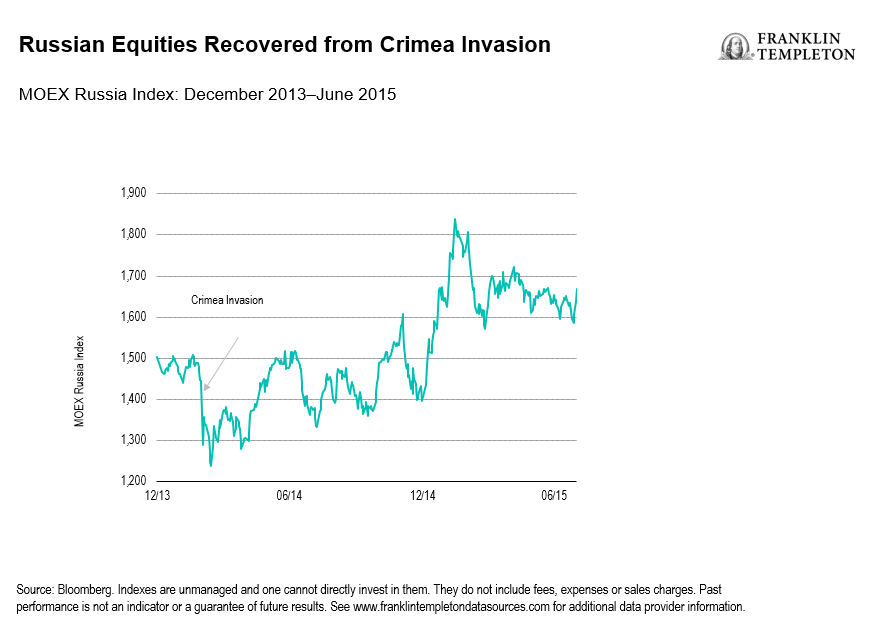

Lessons from prior Russian military action may offer some comfort for investors who share our view. Following the Russian invasion of Crimea in 2014, the MOEX Russia Index fell almost 20%. Within nine months, the index reached a new high, up 30% from the March lows. Short-term investors who reduced their Russian weighting subsequently missed out on a significant rally.

Russia announced its intention to reach net zero by 2060 in the runup to COP 26 (the most recent United Nations Climate Change Conference). Whilst not aligned to the Paris Agreement on climate change, it does signal a clear direction of travel. Engagement is the key to encourage Russia to bring its commitment forward to 2050 as well as setting out goals for 2030. Russia is one of the biggest oil and gas producers globally, it also has vast forests and generates 40% of its power from renewable sources including hydro, nuclear, solar and wind.2 The conflict in Ukraine does not detract from the need for engagement, which we believe is best achieved via ownership of companies that have shown a willingness to decarbonize, as opposed to divestment.

While valuations suggest a lot of risk has already been discounted, a war scenario implies further downside is likely. The Russian equity market currently trades on a very low single digit price-earnings-ratio (P/E). In contrast to the undemanding P/E, consensus expectations for Russia’s return-on-equity in 2022 is 15%, above its long-term average as well as that of emerging markets, which is 13%.3 It is, however, a very dynamic and fluid situation with the conflict likely to be long and drawn out.

Oil prices have spiked higher and gas prices are rising, which is inflationary in the short term and could result in stagflation if central banks raise interest rates too aggressively. Russia and Ukraine are major agricultural exporters of wheat and oil seeds. Russia and Belarus are the second and third largest producers of potash fertilizer. Belarusian potash exports are already sanctioned, which if combined with weaker supply of wheat from Ukraine, has global inflationary implications.

Uncharted Territory

Markets are entering uncharted territory in terms of the implications of a war on Europe’s borders. The conflict between Ukraine and Russia could draw in other countries and NATO, or the war could be short, but the occupation long. In the coming days and weeks, investors will be weighing a range of topics including the implications for hard and soft commodities, and whether the current global inflationary wave will give way to deflation as global demand weakens in a prolonged conflict scenario. Global central banks will be reassessing the implications for demand and whether they will need to recalibrate their monetary policy guidance.

A prolonged conflict will likely have implications for the geopolitical order and the shape of European borders for years to come, elevating the equity risk premium across developed and developing markets. Investors will be closely watching the US response as well as how Beijing reacts, given its policy of non-interference in the internal affairs of other countries and the implications for its Taiwan policy.

We retain conviction in our Russian equities, as long as sanctions/tensions do not a) bar us from owning Russian stocks, or b) significantly increase costs associated with the ownership of specific securities.

Positive View on Russian Exposure |

|

Negative View on Russian Exposure |

|

|

What Are the Risks?

All investments involve risks, including the possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realised. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

________________

1. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.

2. Source: BP Statistical Review of World Energy 2021.

3. Source: Bloomberg, as of February 24, 2022.

4. Source: Bloomberg, as of February 2022. Long-term average = 10-yr period from 2012 to 2021 of 7%.

5. Source: Bloomberg, as of February 24, 2022. There is no assurance that any estimate, forecast or projection will be realized.

6. Source: IMF World Economic Outlook Database, data for Russia as of 2020.

7. Sources: Bloomberg, Central Bank of the Russian Federation. FX figure as of December 31, 2021, and includes gold.