English

English Español

Español

This post is also available in: Spanish

by Franklin Templeton Emerging Markets Equity

Key Takeaways

-

- The Russia-Ukraine conflict has weighed on global equity markets, with the exception of Brazil.

- Surging commodity prices benefit Brazil, the fourth-biggest commodity exporter globally.

- Ample renewable energy resources could shield Brazilian farmers from higher energy and fertilizer costs.

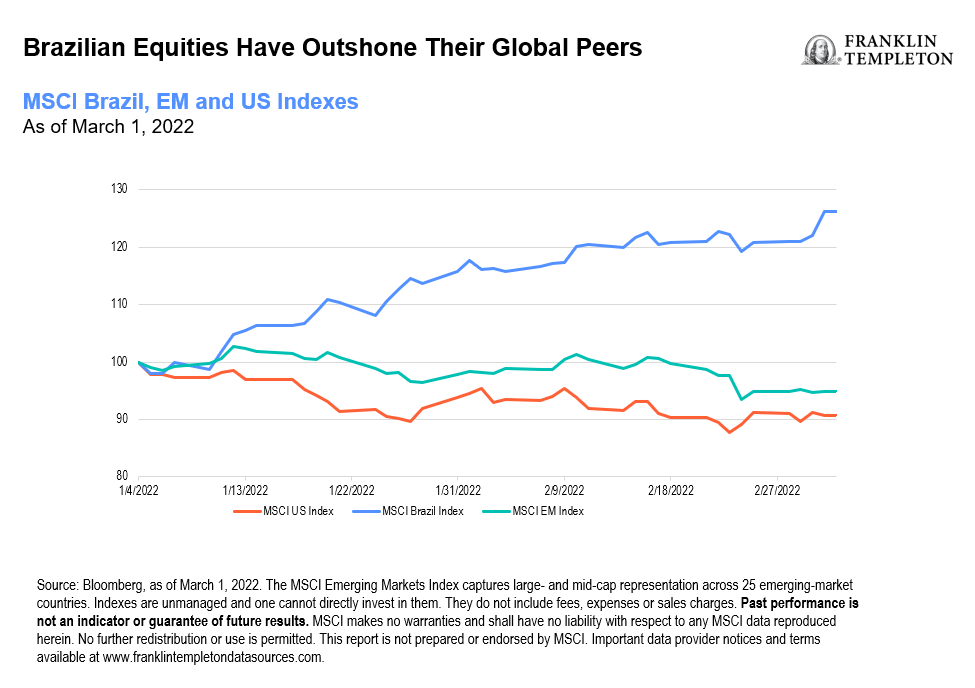

Brazilian Equities Rally on Higher Commodity Prices

Brazil defied the global market rout in February to end the month higher. The MSCI Brazil Index rose 18% in the first two months of the year, outperforming the MSCI Emerging Markets (EM) Index and the MSCI US Index.1 The increase in energy, industrial and agriculture commodities prices this year is benefiting the MSCI Brazil index, which has a 45% weighting in these sectors. Easing concerns over the outcome of the presidential election in October have reduced the risks for the market in the eyes of investors.

While the impact of geopolitical tensions remains difficult to predict for now, Brazil stands out to us as one of the potential beneficiaries of sanctions against Russia.

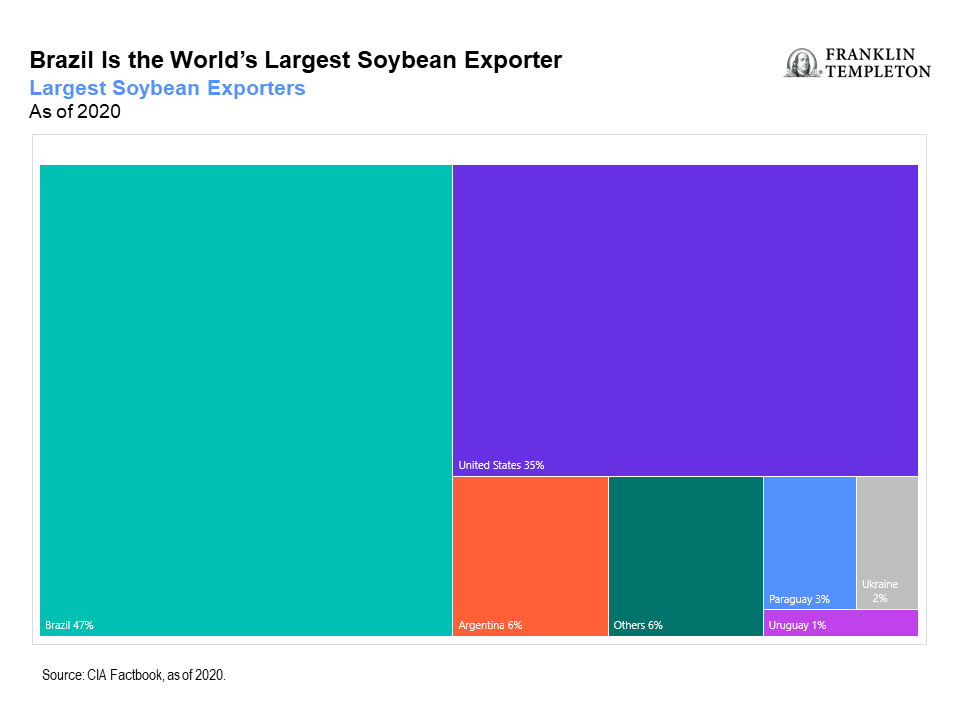

The World’s Fourth-Largest Commodity Exporter

Brazil is the world’s fourth-largest commodity exporter. It is the biggest exporter of soybeans and coffee, and the second-biggest exporter of corn and iron ore.2 The continuation of last year’s commodity price surge amid global supply concerns from the Russia-Ukraine conflict is potentially good news for Brazil’s commodity exports, economy and market.

Agricultural commodity prices surged 18% in the first two months of the year, driven by geopolitical uncertainty, adding to their 25% gain in 2021.3 We expect this rally to be a tailwind for Brazil given its status as a commodity exporter.

Brazil, like many other agricultural exporters, could face higher fertilizer prices and energy costs due to the Russia-Ukraine conflict. Russia and Belarus are the second- and third-largest potash producers globally, with the latter’s potash exports already sanctioned. Potash is a key agricultural fertilizer.

However, Brazil may have a competitive edge over other agricultural exporters. The country generates 80% of electricity through renewable sources, shielding it from higher prices for carbon-intensive electricity production. In addition, its ample domestic supply of animal feed could prove advantageous amid rising global energy and soybean prices.4

China and the United States are Brazil’s largest export partners. The two countries account for 28% and 13% of Brazil’s total exports respectively, while Russia’s share is under 1%.5

Earnings and Valuation Support

The energy, materials and agricultural sectors account for 45% of the MSCI Brazil Index. Surging commodity prices are leading analysts to raise earnings forecasts in Brazil. The consensus estimate for 12-month forward earnings per share in Brazil is up 6% year-to-date.6

Despite the stock market’s recent climb, valuations look appealing. The MSCI Brazil Index’s price-to-earnings ratio of 8x on a 12-month forward basis remains at a discount to its 15-year average of 11x.7

Potential Risks

-

-

- The US Federal Reserve has signaled its intention to tighten monetary policy amid rising inflation.

- A decline in commodity prices could weaken the investment case for Brazil.

- The lead-up to the country’s presidential election in October is likely to come with political noise.

-

In these uncertain times, we think that Brazil, with its abundant supply of commodities, favorable corporate earnings momentum, and undemanding equity valuations, deserves greater attention from investors.

What Are the Risks?

All investments involve risks, including the possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realised. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

______________________________

1. Source: Bloomberg, as of March 1, 2022. The MSCI Emerging Markets Index captures large- and mid-cap representation across 25 emerging-market countries. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

2. Source: CIA World Factbook 2020.

3.Source: S&P GSCI Agriculture Index.

4. Source: Government of Brazil, “Renewable energy sources represent 83% of the Brazilian electricity matrix,” January 28, 2020.

5. Source: World Integrated Trade Solution, latest available data as of 2019.

6. Source: Bloomberg, as of March 1, 2022.

7. Source: Bloomberg, as of March 1, 2022.