English

English Français

Français Italiano

Italiano Español

EspañolThis post is also available in: French, Italian, Spanish

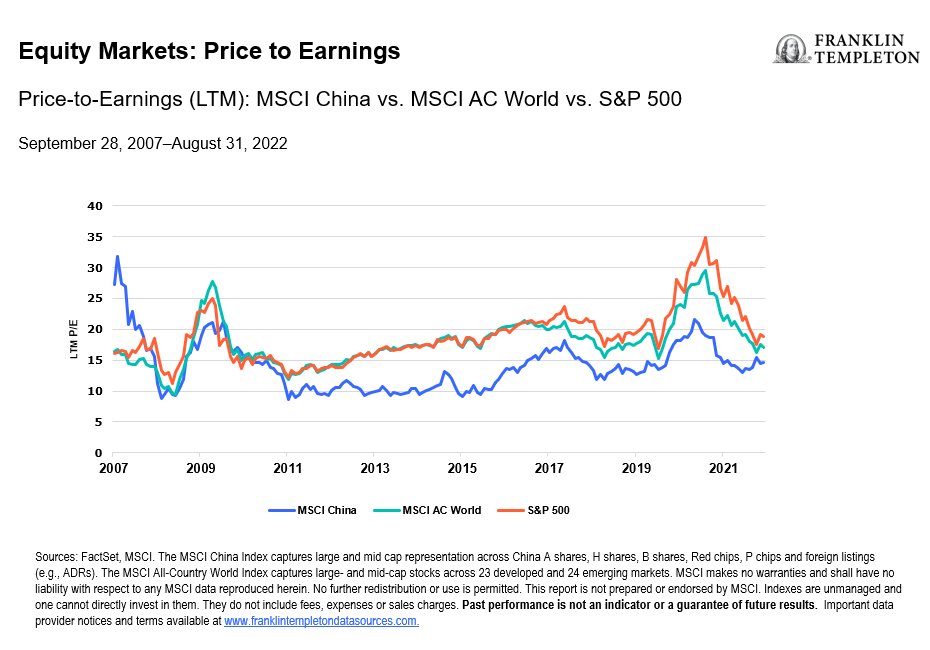

In our analysis, investor sentiment and valuation in Chinese equities are currently at unsustainable lows. As such, we are positive on the relative case for the Chinese equity market’s prospects as we move into the latter part of this year. While we can expect the realization of some degree of slowing growth, policy tools are available to underpin the economy so it should not be fully derailed.

Positive catalysts for market recovery

We have identified several positive catalysts that could help China’s market recover. These include an easing of zero-COVID restrictions, a reduction in geopolitical tensions and clear evidence of no further tightening in the regulatory environment. We see reasons for optimism in each area. The government is likely to continually adjust COVID-19 policies—driving greater economic resilience and flexibility in the face of localized restrictions—and utilize flexible policy tools. We anticipate stabilization in earnings revisions, and a regulatory shift toward implementing previously announced policies vs. incremental new tightening measures.

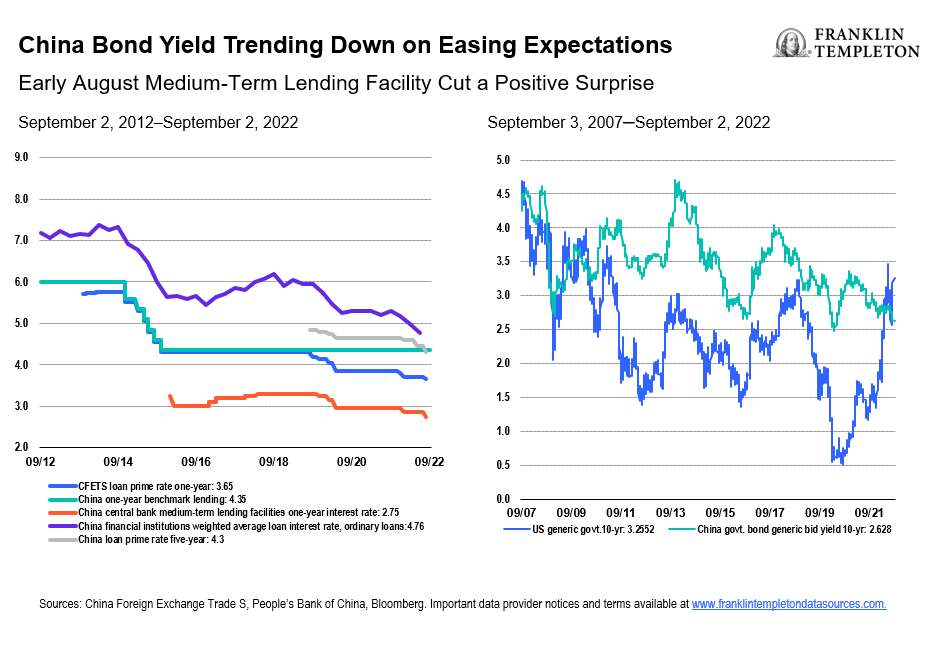

As seen in the charts below, monetary policy in China has followed a different trajectory from the United States and other major central banks, as interest rates in China have been trending lower, with 10-year yields in the United States now higher than in China for the first time in over a decade.

Opportunities arising from government long-term goals

We believe areas aligned with the government’s long-term goals offer the most opportunities for investors. Common prosperity, for instance, could expand the aggregate size of disposable income and support social welfare as lower-tier cities remain a large untapped market for many consumer products and services. Green development, with orderly decarbonization to avoid disruption to economic growth, should enable Chinese companies to secure global leadership in supply chains spanning from new energy vehicles (NEVs) to solar.

In our view, sectors with high exposure to NEVs, solar, wind power and energy storage have upside potential due to strong NEV growth momentum, high energy prices, the ongoing Russia-Ukraine war and government subsidies. In addition, gaining independence from imports through domestic substitution in key technologies, such as semiconductors, represents a huge growth opportunity with strategic benefits. Putting this in context, China imported over US$400 billion in semiconductors in 2021.

Other opportunities can be found in high-quality internet companies that have seen valuations crash, yet they have vast amounts of cash on their balance sheets, are improving their cost efficiencies and are returning cash to shareholders.

Sectors and companies where we see risks

In our opinion, risks exist in industries characterized by oversupply and excess leverage (such as property developers) and restricted earnings growth and returns to shareholders (such as utilities managed for public benefit, not for minority investors). We see companies with weak cash flows that are reliant on fundraising to support business operations as vulnerable due to a lower risk appetite. We also expect sectors with high consumer exposure to be under pressure in the next few quarters due to low consumer confidence and weak demand.

We will continue to search for opportunities in the Chinese equity market as we actively manage our portfolios based on bottom-up company research and top-down macroeconomic and policy monitoring. We retain long term optimism towards China’s market.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with investing in foreign securities, including risks associated with political and economic developments, trading practices, availability of information, limited markets and currency exchange rate fluctuations and policies; investments in emerging markets involve heightened risks related to the same factors. Investments in fast-growing industries like the technology and health care sectors (which have historically been volatile) could result in increased price fluctuation, especially over the short term, due to the rapid pace of product change and development and changes in government regulation of companies emphasizing scientific or technological advancement or regulatory approval for new drugs and medical instruments. China may be subject to considerable degrees of economic, political and social instability. Investments in securities of Chinese issuers involve risks that are specific to China, including certain legal, regulatory, political and economic risks.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.