English

English Français

Français Español

Español

This post is also available in: French, Spanish

Key takeaways:

- Emerging markets remain resilient despite headwinds, but many investors have shied away from the asset class.

- We believe emerging markets are better positioned to weather current challenges versus developed markets due to factors including effective monetary policy and low debt.

- Companies in emerging markets are trading at attractive valuations and have offered solid dividend yields.

- We are increasingly optimistic on the long-term prospects for emerging markets equities at current prices.

Emerging markets resilient despite headwinds

Global economies have faced a number of challenges in recent months, leading to depressed stock market returns. The ongoing Russia-Ukraine war continues to have ripple effects on the global economy. And although most countries have gone back to business as usual following the peak of the COVID-19 pandemic, the virus is probably not going to fully disappear. In addition, China’s “Zero-COVID” policy has been weighing on economic activity there. Other well-known market challenges include rising inflation and interest rates, as well as the surging US dollar.

Despite these headwinds, emerging economies continue to prove their resilience. We believe it is now a compelling time to consider emerging markets equities, even as many investors are less focused on the asset class.

Conventional and consistent policies

Policies in emerging markets have generally been more conventional and consistent than those of developed markets, which we believe will ultimately lead to more robust economies relative to their own history and relative to developed markets. In contrast to developed markets in the post-global financial crisis period, emerging economies did not experiment with negative interest rates. They have generally had upward-sloping, traditional yield curves over the past decade. During the recent pandemic, policymakers in emerging markets generally did not pursue very aggressive fiscal support plans, which means they did not blow up their sovereign balance sheets. Contrast this with developed markets like the United Kingdom, for example, which pursued aggressive fiscal expansions.

As inflation began to accelerate post-pandemic, emerging economies were also preemptive in tightening interest rates. Thus, while the United Kingdom, the eurozone and the United States are still trying to catch up with rising inflation, many emerging economies have largely completed their tightening cycles. Brazil, for example, started tightening in March 2021, and has made 12 consecutive rate hikes. Inflation has been decelerating there in recent months, leading the central bank to pause its hiking cycle in September. The US Federal Reserve, meanwhile, did not start raising rates until March of 2022.

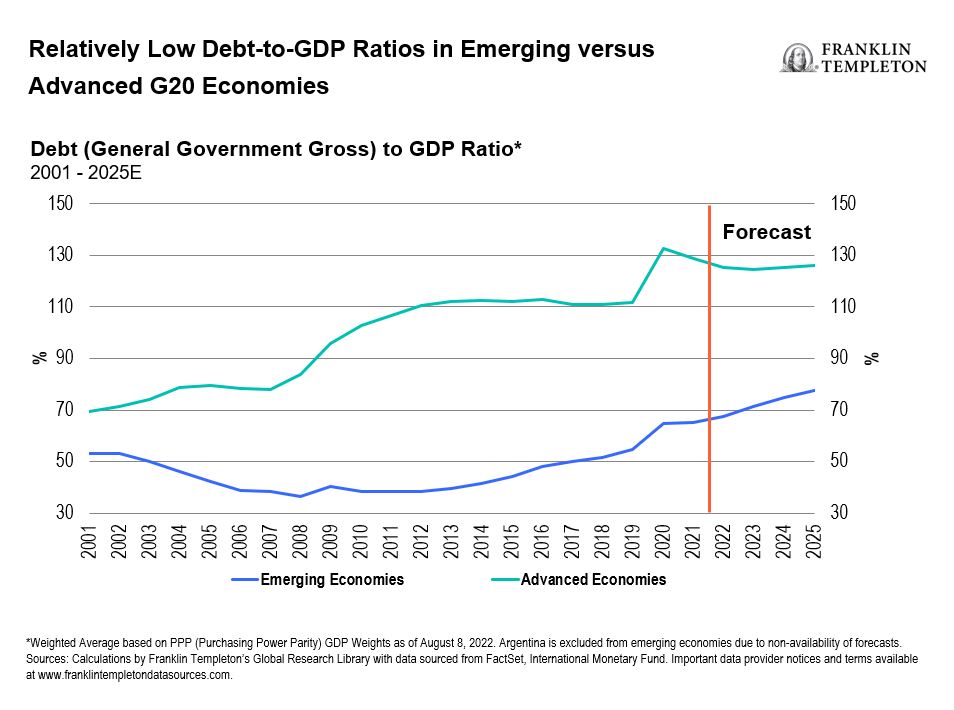

In addition, emerging economies are typically less leveraged at the sovereign, corporate and household levels. For example, in Mexico, the household debt-to-gross domestic product (GDP) ratio is only 16%, compared with the United Kingdom’s ratio of around 90%.1

At the stock level, emerging markets offer investors opportunities in high-quality and high-growth companies. They are home to some of the most innovative, technology-oriented companies in the world—companies that are building the digital architecture around us. These include hardware and software suppliers as well as semiconductor manufacturers. Some are even responsible for the transition to decarbonization. Many emerging market companies are global leaders in the production of electric vehicles and electric batteries, and in renewable energy such as in solar manufacturing.

Attractive valuations

Emerging market equity valuations are trading at near historic discounts versus the developed world. In our analysis, the relative profitability between these two asset classes does not warrant the current 45% discount on a price-to-book basis.2

Also, relative to its own 15- to 20-year history, emerging markets as an asset class is one of the few that looks cheap to us. The MSCI Emerging Markets (EM) Index, a benchmark representing the asset class, is now trading at close to 10 times forward earnings, compared to around 18 times for the US S&P 500 Index (S&P 500).3

Increased dividends and buybacks

Emerging market companies have recently been increasing their dividends. They have been using their cash flows to distribute dividends to shareholders rather than deploying capital given uncertain growth outlooks. Company managements have also been seeing value in their equities, resulting in increased buyback activity. In our opinion, these increases are temporary. In this volatile environment, these dividends and buybacks are appreciated, but we would prefer companies invest in their own businesses for secular growth opportunities.

While we believe the persistence of high dividend levels is unlikely to remain at the current 4% level, there has been a sea change in how emerging market companies think about capital optimization and balance sheet management.4 Over the past 20 years, approximately 2.5% of annualized total returns of 9% have come from dividends.5 Thus, there has been dividend support to the asset class, which many investors may not realize.

Increasing optimism

Over the long term, we are increasingly optimistic about emerging market economies. Despite the current environment of slowing growth, rising inflation and geopolitical issues globally, we have confidence in both the emerging markets asset class and our strategies. We continue to seek high-quality business with solid balance sheets, competitive advantages and attractive valuations.

WHAT ARE THE RISKS?

All investments involve risks, including the possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size and lesser liquidity. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments. China may be subject to considerable degrees of economic, political and social instability. Investments in securities of Chinese issuers involve risks that are specific to China, including certain legal, regulatory, political and economic risks.

Franklin Templeton and our Specialist Investment Managers have certain environmental, sustainability and governance (ESG) goals or capabilities; however, not all strategies are managed to “ESG” oriented objectives.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

__________

1. Sources: CEIC, “Mexico Household Debt: % of GDP,” June 2022. CEIC, “United Kingdom Household Debt: % of GDP,” June 2022.

2. Source: Factset. Price-to-book ratio is a financial ratio used to compare a company’s current market value to its book value.

3. Sources: MSCI, Nasdaq. The MSCI EM Index is a free float-adjusted, market capitalization-weighted index designed to measure the equity market performance of global emerging markets. The S&P 500 is a market capitalization-weighted index of 500 stocks designed to measure total U.S. equity market performance. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator of future results. See www.franklintempletondatasources.com for additional data provider information.

4. Source: Factset.

5. Source: Factset, FTEME.